The Underwriter wants to know everything about you — let’s learn more about them.

The Who

Insurance underwriters are trained to identify, understand and prevent risks in either life, health, or property and casualty insurance. Property and casualty is a broad field that can include business, home or auto insurance. Their specialized risk assessment knowledge enables them to determine whether they will insure something or someone and for how much. Underwriters decide whether to agree to be financially responsible to the insured if something unexpected or catastrophic happens related to the policy.

So, the underwriter decides if you are worth a monetary risk to cover you and how much premium will be charged if approved.

The What

The U.S. Bureau of Labor Statistics describes what an underwriter does as follows:

Analyzing insurance applications

Identifying the risks of insuring applicants

Screening applicants based on a specific set of criteria

Evaluating recommendations from underwriting software

Contacting field representatives, healthcare providers, and others for more data

Deciding whether to offer insurance

Determining appropriate premiums and amounts of coverage

Reviewing and updating the rules for automation software

The difference between the specialties lies in the criteria used to make the decision. For life insurance, examples of the criteria are age and financial history. For health, the main criteria are medical history and age. For auto insurance, underwriters look at driving record, age and type of vehicle. In everything they do, insurance underwriters must strike a balance between risk and caution. Too much risk means the insurance company will pay out too many claims. Too much caution and the carrier will not make enough money from premiums.

The Where

Underwriters work for insurance companies and can usually be found at desk in the company headquarters or a regional office. They use software systems to analyze and rate insurance applications, make recommendations based on risk, and adjust premium rates according to the risk. Sometimes they might work overtime or on weekends, depending on the type of underwriting, and they may inspect the property or vehicle in person. The average salary has been on the rise over the years and depends upon qualifications, education, experience and location.

The How

Insurance underwriters use a software program to recommend coverage and premiums based on the specific data provided by the applicant, and will approve or reject the application after an evaluation of the software results. For simple and common types of policies, such as those for automobile or homeowners’ insurance, the automated recommendations are commonly followed.

For more complicated types of insurance, such as workers’ compensation or business income, underwriters rely on analytical insight and experience. For example, in some cases, a reported bankruptcy or cancer treatment might impact a policy so they will review other sources such as medical records and credit scores.

The How To (become an underwriter)

{from kaplanfinancial.com}

“In general, to become an insurance underwriter, you should have excellent decision-making and mathematical skills, strong analytical and computer skills, and good interpersonal skills. You should also be detail-oriented. You’ll need a bachelor’s degree at a minimum. You do not have to be a finance or business major; however, you should plan to complete mathematics, economics, finance, and business courses. Unlike insurance agents and financial representatives who sell insurance as an investment, you do not have to have a license to become an underwriter. However, in some of the larger insurers, having an insurance license can help you stand out in a group of prospective trainees or associates.

Underwriters who are just starting out are usually required to be an associate for an established underwriter, learning about basic applications and common risk factors on the job. As they become more experienced, they begin to work more independently, and their work becomes more complex. Also, big insurance firms often offer comprehensive training for new hires. Eventually, they no longer need supervision and will work independently as underwriters. Most underwriters participate in underwriting professional development to sharpen their skills and knowledge.”

The Why

The role of an insurance underwriter includes responsibilities such as:

Evaluating information about the potential client (i.e., age, marital status, medical history, driving record, etc.)

Using underwriting software to analyze the risk profile of the potential client

Deciding whether or not insurance coverage should be offered to an individual

Calculating costs to provide coverage and establish the pricing for the premium

Developing solutions to reduce the risk of paying future insurance claims

Analyzing actuarial tables, which is the data provided by actuaries

Although some of the work is automated and is carried out by insurance software, as mentioned above, an underwriter will still be involved with a potential client if a change in risks or change in the conditions of the insurance policy is likely. The underwriter will determine whether or not the insurance company would like to continue with providing insurance coverage or if it will establish new insurance terms with the client.

The End, but actually the beginning

The term underwriter first emerged in the early days of marine insurance. Shipowners sought insurance for a ship and its cargo to protect themselves if the boat and its contents were lost. Shipowners would prepare a document that described their ship, its contents, crew, and destination and go to the local hangout or pub, usually.

An agreed-upon rate and terms were set out in the paper. Business people who wished to assume some obligation or risk would sign their name at the bottom and indicate how much exposure ($) they were willing to accept. These businessmen became known as underwriters. They would get a return on their investment or help cover the loss in the event of an accident.

This post is for the intrepid traveler daring to leave their house.

Disclosure: I’ve never purchased travel insurance. I almost did when I took my daughter to NYC for her 18th birthday in 2020–January, mind you–but I made sure the arrangements were all refundable by a certain date. The fact that the city shut down less than two months later because of a pandemic would have been unimaginable, and has prompted travelers to take precautions they might not have otherwise. Here’s a primer on travel insurance.

I was more concerned about weather delays in NYC January 17-19, 2020.

Travel insurance is coverage designed to protect against risks and financial losses that could happen while traveling–from minor inconveniences like missed airline connections and delayed luggage to more serious issues including injuries or major illness. As we know, Covid-19 has shoved the elephant out of the room, so I’ll begin with FAQ regarding travel insurance coverage and cancellation for illness.

Does Travel Insurance Cover the Coronavirus Pandemic?

On January 21, 2020, the Coronavirus disease 2019 (COVID-19) became a named event, which affects the travel insurance coverage available for new policies purchased thereafter because it is known. Insurance is designed to protect you from an unpredictable or spontaneous loss. For example, if a hurricane ruins your trip, travel insurance would only cover you if you bought it before the hurricane formed. Be sure to purchase insurance as early as possible and always read the fine print no matter what policy you choose.

Comprehensive travel insurance

This is the typical policy that people imagine when they think of trip insurance. The comprehensive policy usually covers delays, cancellation due to sickness or death, lost luggage and some emergency medical costs.

Benefits included in comprehensive coverage may apply in the following unforeseen scenarios:

Emergency Medical Coverage: a sick traveler must see a doctor and/or go to the hospital during a trip.

Emergency Medical Evacuation Coverage: in rare cases, a sick traveler requires an emergency medical evacuation to the nearest appropriate hospital or back home for recuperation.

Trip Interruption: an extremely sick traveler cannot continue with a trip and must return home.

Cancel For Any Reason: Currently, if you are looking for trip cancellation coverage because you are concerned about the coronavirus, you will now need to purchase a plan that includes Cancel For Any Reason since the travel warnings are now foreseen. This benefit is time-sensitive and has other eligibility requirements, so not all travelers will qualify.

Some plans may exclude epidemics/pandemics and may not provide coverage for related issues. Please be sure to read the plan details carefully before purchasing.

Over the course of the coronavirus pandemic, many traditional travel insurance companies have expanded or adapted their existing coverage for travelers. In addition to the coverages above, examples of these may include:

Reimbursement for covered medical treatment during a trip due to a COVID-19 illness

Get sick with COVID-19 and must cancel a trip by physician’s order

Physician orders a quarantine before trip

Lost a job during the coronavirus pandemic by no-fault of your own

Cancel For Any Reason (CFAR) offers the most trip cancellation flexibility and is the only option available to cover fear of travel. CFAR is an optional, time-sensitive benefit with eligibility requirements, so not all travelers will qualify. Full terms of coverage will be listed in state-specific policy. If eligibility requirements are met, reimbursement is up to 50%-70% of the insured prepaid non-refundable trip cost.

InsureMyTrip.com

Does Emergency Medical Coverage Travel with You?

Some travel insurance plans do offer emergency medical benefits if you need a doctor or hospital visit during a trip. Check your personal health insurance plan first to understand coverage already in place. However, most health insurance plans don’t provide full coverage in foreign countries and some health plans provide no coverage at all. Travel insurance works in addition to your everyday health insurance and can help supplement medical costs if you get sick or injured before or during your vacation.

If you have Medicare or Medicaid, be aware that medical costs overseas are generally not covered.

Before purchasing a policy, it is imperative to read the policy provisions to see what exclusions apply, such as preexisting medical conditions, and do not assume that the new coverage mirrors that of an existing plan.

Emergency medical coverage may be redundant. Most health insurance companies pay “customary and reasonable” hospital costs if you become sick or injured while traveling, but few will pay for a medical evacuation.

From InsureMyTrip.com, medical plans and coverage to consider include:

Travel Medical Insurance is offered either as part of comprehensive travel insurance plans or can be purchased as a stand-alone plan. These plans only offer coverage while traveling outside of your home country. Contact your regular health insurance provider to inquire about global benefits and how your benefits apply when you are outside of your home country.

Emergency Medical Evacuation Coverage provides transport assistance in the event that you become seriously ill or injured while traveling. Generally, these plans provide emergency medical evacuation to the nearest appropriate care facility if the assistance company and the physician feel you’d be better suited at a different facility. For those who want to ensure transport to the hospital of their choice, travelers may want to consider also purchasing an air medical transport membership. If hospitalized during your trip, this membership may provide transport to a hospital of your choice, often closer to home, without it being determined as “medically necessary” as required on typical travel insurance plans. (For medical transport memberships, some destination restrictions may apply for evacuations related to COVID-19.)

Trip Interruption Coverage is included in travel insurance comprehensive plans. It’s a benefit that offers travelers reimbursement of their pre-paid, non-refundable expenses should they unexpectedly need to cut their travels short. However, there are exclusions for this, so be sure to review your policy carefully.

Travel insurance can help cover expenses stemming from lost or stolen luggage. This is especially useful if an airline loses your bags, as it can be very difficult to get them to pay for lost luggage. In the United States, the Department of Transportation (DOT) requires airlines to compensate fliers up to $3,300 for lost baggage. In foreign countries that amount is a maximum of $1,750. But to receive those maximum amounts, passengers must provide receipts proving the value of the lost bags and their contents. And some airlines require that the claim be filed within 21 days.

To make matter worse, DOT doesn’t define when baggage is officially lost (as opposed to just “delayed”). Overseas, a bag is only considered “lost” after 21 days. For delayed bags, DOT only requires airlines to provide victims with enough money to buy necessities like clothing, medicine and toiletries.

The possibility of baggage and personal belongings being lost, stolen, or damaged is a frequent travel problem. Many travel insurance policies pay for belongings only after you exhaust all other available claims. Your homeowners or renters insurance may extend coverage outside of your domicile, and airlines and cruise lines are responsible for loss and damage to your baggage during transport. Also, credit cards may provide automatic protection for things like delays and baggage or rental car accidents if used for deposits or other trip-related expenses.

What if. . . Plans Change

Travel insurance can help cover costs stemming from trip cancellations. Most resorts or cruise lines won’t give you a full refund in the event of a cancellation. If you cancel two weeks or more before your trip, most resorts will at least charge a cancellation fee; many cruise lines might only give you a 25% refund or will give you partial credit on another cruise. If you cancel within two weeks of a trip, with most companies you won’t give any refund whatsoever. Unforeseen circumstances happen, and you want to be covered just in case.

Before looking into travel insurance, think about the reasons you might cancel. Is a trip delay due to weather going to dramatically change your vacation? Is it possible your school year will be extended, or you will need to take a work-related trip instead? Are there acts of war in the country you’re going to visit? Are you nervous about the CDC issuing a travel warning for your vacation destination?

These are all valid reasons, but not all travel insurance covers these concerns. When booking a pricey trip, investigate insurance at the same time. Some policies require you buy travel insurance within a certain amount of time after making your initial trip payment, such as within 10 to 30 days.

Purchasing Travel Insurance

Travel insurance will vary by the provider on cost, exclusions, and coverage. Be sure to read all disclosure statements and check what protections your credit card might offer.

Coverage is available for single, multiple, and yearly travel. Per-trip coverage protects a single trip and is ideal for people who travel occasionally. Multi-trip coverage protects numerous trips occurring in one year, but none of the excursions can exceed 30 days. Annual coverage is for frequent travelers. It protects for a full year.

Premiums are based on the type of coverage provided, a traveler’s age, the destination, the duration, and the cost of your trip. Standard per-trip policies cost between 4% to 10% of the trip’s cost. Specialized policy riders focus on the needs of business travelers, athletes, and expatriates (i.e. working overseas).

Also, it is suggested that a traveler register travel plans with the State Department through its free travel registration website. The nearest embassy or consulate can contact them if there is a family, state or national emergency.

Worthy travel insurance plans always include the following provisions:

Coverage for most countries in the world (including the places you plan on visiting).

Some coverage for your electronics (and have the option for a higher coverage limit).

Coverage for injury and sudden illnesses.

Offer 24/7 assistance (you don’t want to call to be told to call back later).

Coverage for lost, damaged, or stolen possessions like jewelry, baggage, documents, etc.

Coverage for cancellations for hotels, flights, and other transportation bookings if you have a sudden illness, death in the family, or some other emergency.

Coverage for political emergencies, natural disasters, or strife in the country that cause you to head home early.

Financial protection if any company you are using goes bankrupt and you are stuck in another country.

Recommended online agencies for the best service and value are:

Just as important as knowing what your plan covers is knowing what it doesn’t cover. Generally speaking, most plans don’t cover:

Accidents sustained while participating in extreme adventure activities such as hang gliding, paragliding, or bungee jumping (unless you pay for extra coverage).

Alcohol- or drug-related incidents.

Carelessness in handling your possessions and baggage.

Recklessness (how “reckless” is defined is a matter up to each company).

Pre-existing conditions or general check-ups. For example, if you have diabetes and need to buy more insulin, you won’t be covered. If you want to go see a doctor for a general check-up, you aren’t covered either.

Lost or stolen cash.

Your theft coverage won’t cover you if you left something in plain sight or unattended.

If civil unrest makes your destination unsafe but your government hasn’t called for an evacuation, you’re probably out of luck too.

Options to include:

Payment for expenses if you get sick or injured on a trip

Travel medical and accident coverage

To be taken to the nearest hospital or flown home if necessary

Emergency evacuation and repatriation

Reimbursement if you get sick and have to cancel or end your trip early

Trip cancellation AND trip interruption

Payment for lost, stolen or damaged luggage or goods

I believe travel is good for the soul, and travel insurance is good for peace of mind. Look into the options, talk to your agent, and decide whether it’s worth it to you.

To protect yourself and other drivers, you must carry liability and uninsured motorist insurance in Tennessee.

It’s expensive and there are so many more things you’d rather spend money on than auto insurance, but if you get pulled over or in an accident, the officer is going to ask for three things: License, registration and proof of insurance.

If you are caught driving without insurance in Tennessee, you may be charged with a Class C misdemeanor, which can result in fines or a suspended driver’s license requiring an SR-22 form to be reinstated. Ignoring the law to save money could end up costing you a whole lot more.

Since 2017, uninsured drivers in Tennessee will pay fines and risk losing their vehicle registration if they are unable to demonstrate proof of financial responsibility. A web-based program will verify insurance for all Tennessee drivers. These changes come as part of the James Lee Atwood Jr. Law.

If you are involved in an accident while uninsured, your charge will be bumped up to a Class A misdemeanor. Penalties for driving without insurance can include:

A fine of $300

The revocation of your driver’s license until you:

Provide proof of insurance, and

Retake and pass your driver’s license examination

A restoration fee of $65 to get your license back

A $50 fee to be paid to the commissioner of safety

The requirement to provide proof of insurance with an SR-22 certificate for three years

Despite these consequences, about 20% of all motorists in this state are driving uninsured vehicles. This is much higher than the national rate of 13%.

In the state of Tennessee, your car insurance policy must include the following:

Liability insurance: This covers injuries and damage you may cause to others if you are responsible for a collision. You must have at least the following amounts of coverage:

Bodily injury liability coverage: $25,000 per person / $50,000 per accident

Property damage liability coverage: $15,000

Uninsured motorist insurance: This covers your injuries and property damage if you are in an accident caused by an uninsured, underinsured or hit-and-run driver. You must have at least the following amounts of coverage:

Bodily injury coverage: $25,000 per person / $50,000 per accident

Property damage coverage: $15,000

In addition to the mandatory coverage, most car insurance providers offer a variety of coverage options that you may want to consider. These include:

Collision coverage: This covers collision-related damage to your own vehicle, regardless of fault. Pays to repair or replace your car if it is damaged in a collision with another vehicle or a stationary object. It can also cover you if you overturn your vehicle while making a sharp turn. It is often required by lenders until you have paid off your vehicle.

Comprehensive coverage: This covers non-collision-related damage to your own vehicle if it is lost or damaged due to an event such as a falling object, flood, structure fire, hailstorm, or property crime including car theft. This is also typically required by lenders until you have paid off your vehicle.

Medical payments coverage aka Personal injury protection (PIP): This provides coverage for your own medical bills if you (and your passengers) are injured in an accident, regardless of fault.

Towing and roadside assistance: This covers the cost of assistance if your vehicle becomes disabled while you are out on the road, such as if your engine overheats or you get a flat tire.

Rental car reimbursement: This can cover the cost to rent a vehicle while your own vehicle is being repaired following a covered event.

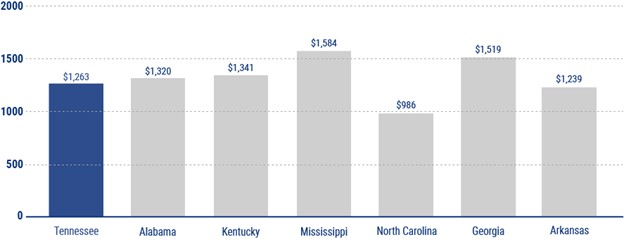

Vehicle owners in Tennessee pay an average of $1,186 per year for their auto insurance coverage. This is lower than the national average of $1,311. Your actual quoted price for coverage will be calculated based on factors such as the make, model, trim, and year of your car, and even personal details like your driving history, age, occupation, and credit score. Comparing quotes from a variety of insurers lets you be sure that you are getting the coverage you want at a competitive price.

Car insurance policies in Tennessee generally follow the car rather than the individual. For example, if you get in a car accident while driving a friend’s vehicle, the primary source of the compensation would be your friend’s auto insurance coverage, not your own.

Tennessee is not a no-fault state.

This means that if you are in a collision, the person responsible for the accident is responsible for covering any resultant property damage and necessary medical treatment. If the at-fault driver does not have enough insurance to cover the costs, they will be expected to make up the difference out of pocket.

In no-fault states, your own insurance policy provides the first line of coverage for necessary medical treatment, regardless of fault.

When seeking to reinstate your driver’s license after being convicted of a DUI, driving without insurance, reckless driving, or another driving violation that results in a suspension, you must file a SR-22 insurance document. This form gives proof of future responsibility, and you might need to have it for five years from the date of the suspension.

According to the Tennessee Department of Safety and Homeland Security, if you file the SR-22 for a total of three years within the five-year period, the SR-22 might be canceled. If five years pass from the date of the suspension before you reinstate your privileges, then you don’ need to file the SR-22. If you cancel the SR-22 before the required time passes and you fail to file a new form, your driving privileges remain suspended.

Your insurance provider may be able to electronically file the SR-22 insurance documents. That way, you can get back on the road quicker, though with a little less cash in the bank.

How do you choose? By looks, by experience, by personality, by clever marketing swag? Consider these questions first.

Now that we’ve all celebrated (or hated) Valentine’s Day, let’s turn our focus to an oft overlooked relationship in our lives: the one with your insurance agent. Quick! What’s his/her name? If you know without looking, that’s a good start, but I should stop here to add that if you don’t know the carrier of your insurance, then you aren’t ready to speed date. You need to take it slow and start at the beginning. The following questions should be asked as soon as introductions are made because the answers could quickly reveal compatibility or lack thereof.

1. What’s your specialty?

At Herron-Connell, we write all lines of insurance: home, auto, life, health, business/commercial, disability, specialty, umbrella and more. You can see how having so many options could spread one person thin on their expertise level, so ask if your needs line up best with their qualifications. You may partner up with more than one person in an agency–it’s not cheating!

2. Are you an Independent Agent or a Direct Broker?

An independent agent is not monogamous. They aren’t committed to one particular insurance company so has a wider range of options and carriers to choose from that would ideally best benefit the customer. They can play the field, to keep the analogy going. A direct broker or a captive agent only represents a specific company, like State Farm, and they cannot shop around for a better rate or other options should you lose coverage or get dropped for multiple claims, for example. Herron-Connell is an independent agency and can mix & match if a combo package isn’t best for home and auto, or different carriers have lower rates in multiple areas.

3. Do I get any discounts?

Everyone wants to save a little money, but this question will also reveal the agent’s knowledge and willingness to help. If you feel like they don’t want to take the extra steps to save you money, or heaven forbid, give you any sort of evil eye, run. This dismissive treatment is a giant red flag flapping in the wind of a customer service desert. Discounts could include a good driver discount, a multi-policy discount for bundling home & auto, a lifestyle change; it is a matter of asking and clicking boxes on the application, not very time-consuming or labor-intensive.

4. What’s your home number?

Just kidding, that’s a little much, but ask what you should do if/when you have a question or need help after office hours. Insurance incidents don’t only occur during the week between 9-5. Whether you have a car accident, need help getting a claim paid or something less urgent but important, your agent should be available and willing. When they are not accessible for any reason, they should provide after-hours contact information so that when you need assistance, you have options.

5. Got any references?

Considering all of the personal information your insurance agent asks you, it is completely reasonable, nay, responsible of you to ask them for client references. They may have nailed the interview or first impression, but what happens the day after. Will they take your call? Will they even remember your name? What others say about them counts much more than what they say about themselves. If the words trustworthy, helpful, knowledgeable never show up, them you should probably ring the bell and move on.

If you aren’t comfortable asking these questions, try emailing them to the prospect. This relationship is important and should not be one-sided. Hopefully, if all goes well, you will only hear from them before time comes for renewal or if you run into them at a ballgame or some place. But, taking the time to ask these questions before you make a long-term commitment can help avoid unnecessary heartache and frustration later.

Insurance provides peace of mind, even for those worried about alien abduction, but sometimes, if you claim it, you gotta prove it.

I’m sure it’s no surprise to hear that people make some crazy claims to insurance companies and others take out policies for unbelievable coverages. Let’s take a look at a few of the stranger things in the insurance world and how companies might investigate such X-Files.

I recall hearing something about Gene Simmons (from the band KISS) insuring his trademark tongue for millions of dollars in the 70s, and also about Tom Jones insuring his voluptuous chest hair for millions of dollars. Both accounts are cringey, but seem to be true, though no tongues or hairs have reportedly been harmed on either of those fellas.

You can insure just about anything you can put a dollar amount on and where there is a risk of monetary loss to the owner of the policy. While you may think someone else is out of their mind, insurance is partly about peace of mind that allows one to rest a little easier that all may not be lost should tragedy strike. Gene Simmons wore so much make-up, would anyone even recognize him if his serpentine tongue weren’t hanging down past his chin? Did the band’s success truly depend on

iPhone photo taken by me (Katie) at a Panic at the Disco concert with lead singer Brendon Urie playing a piano suspended in air by a cable. Worth the risk?

Brendon Urie’s premium to insure his life and those of his concertgoers must be quite high since he plays a “floating” piano that drifts over his audience. I can’t imagine!

Anything can happen during a concert, festival, or other live event, so it’s important to have liability and property insurance that can handle the unexpected. Large crowds, elaborate sets, and lots of equipment mean risks are ever-present.

from ProSightSpecialty.com

I didn’t mean to get stuck on musicians and concerts; you’re probably wondering what’s with the Parking for Aliens Only sign. One, it’s an attention grabber. Two, policies actually exist for people who are fearful of an alien abduction. A U.K.-based insurer has sold more than 30,000 such policies across Europe. Premiums can cost up to $150 per month for $1.5 million in total coverage, according to projectparanormal.org, which is quite high considering the probability of alien abduction ever occurring. Should one ever make a claim, however, definitive proof is required to collect any damages.

Enter the EUO

An EUO is not related to a UFO, and actually seems scarier to me. The acronym stands for examination under oath and is a formal statement taken by the insured describing the events in the matter of their particular claim. EUOs are typically, although not always, conducted by an attorney representing the insurance company. A court reporter will type every question and answer verbatim, and sometimes a videographer will record the proceedings. Examinations under oath usually last only a few hours, but could possibly extend over multiple days depending on the case. It’s a serious matter.

An insured should anticipate questions about the cause and origin of the loss, the financial condition of the insured leading up to the event (motive), the insured’s whereabouts at the time (opportunity), the nature and extent of the loss, particular items claimed to have been damaged or destroyed, and the accuracy of answers provided in the insurance application. Seeking legal counsel would be a prudent move before undertaking this examination, although an EUO is not part of a court proceeding, anything you say can be used should the claim be taken to litigation and the insurance company may deny the claim based on the results of the investigation.

An insurance company’s authority to take an examination under oath comes from the insurance contract, which typically contains a provision, under the section “Duties of the Insured,” that the insured must answer questions under oath when requested by the insurer. Even without such a provision, there is almost always a “duty of cooperation” provision in the policy which would also require the insured’s participation in an examination under oath. If an insured refuses, it could result in the insurance company’s denial of the claim based on its assertion that the insured breached the insurance policy by refusing to cooperate. See Spears v. Tenn. Farmers Mut. Ins. Co., 300 S.W.3d 671 (Tenn. Ct. App. 2009).

FAQs about EUOs:

Are EUOs always required? Not always. EUOs are often demanded when there are red flags for fraud, strange circumstances, large claims, potential problems with the application for insurance, etc.

What do I need to bring? Bring several documents in support of your claim and be prepared to answer questions about those documents and specific questions about the loss by the attorney.

Do I have to cooperate? Yes. Your insurance policy has a section that provides you, as the insured, have a duty to cooperate with your insurance company’s investigation, including submitting to an examination under oath. However, you may not have to answer every question or provide every document, but it is important to know that you need to cooperate with your insurance company as your failure to do so may result in the denial of your claim.

Do I need an attorney? It would help. An attorney experienced with EUOs can prepare you for the types of questions you will face, assist in the gathering (and presenting) of documentation, streamline and coordinate communication with the insurance company, and assist you in making strategic decisions, all of which can impact whether your claim is paid or denied.

Why am I being investigated? Insurance companies send claims into the examination under oath process for a variety of reasons. Some reasons are serious and legitimate, while others seem to be trivial. You may never know exactly why, but stick to the truth and everything should work out.