Happy 2021! Look over these 22 questions to review your home and auto insurance for the new year.

Last year brought enough unwelcomed surprises, don’t let home and auto changes negatively affect your insurance coverage. Review the following questions to make sure your policy covers what you need for 2021 and let’s all have a happy, healthy new year!

Have you completed any renovations or additions to your home/property? (Pool, dock, gazebo, deck, fencing, roof or window replacement, other improvements)

Do you have personal property that should be scheduled? (Jewelry, coins, stamps, artwork, collectibles, etc. are limited in coverage on the standard policy – appraisal required.)

Are you interested in learning more about the following protection?

Umbrella Liability (An additional layer of liability over your home & auto policies)

Flood Insurance Business Insurance Life, Health, or Disability Insurance

This list is just the beginning. Review your policy with your agent each year for a thorough check. We’re happy to answer any questions you might have and provide a complimentary review of your home, auto, life, health or commercial insurance policies at Herron-Connell. Give us a call at 865-483-8483.

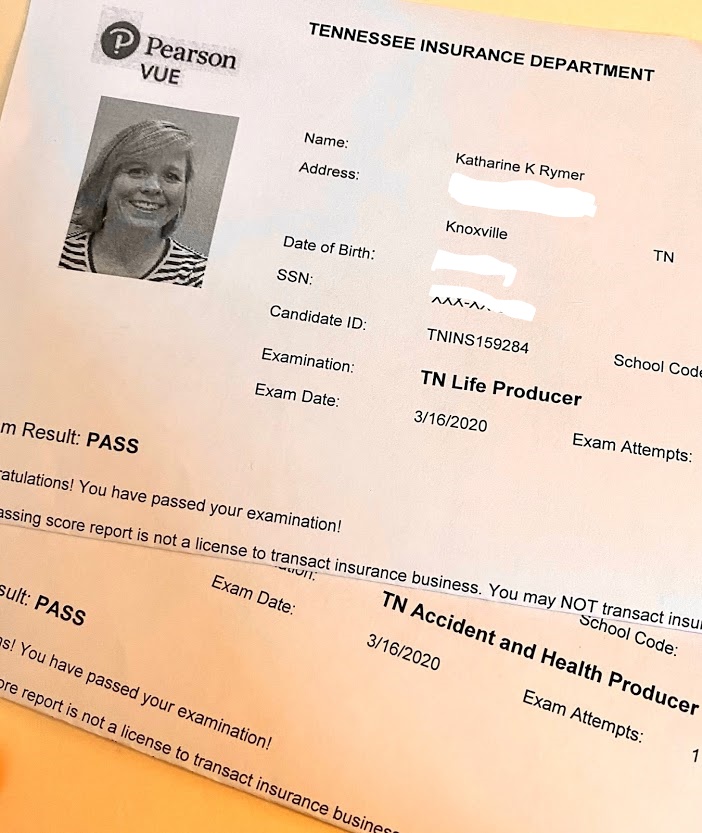

The first steps of becoming an insurance agent in Tennessee.

Disclaimer: I am not an expert or trained in any way to instruct others. This is purely my experience of studying for and acquiring my licenses in Property, Casualty, Life, Accident & Health this past spring.

I went overboard in my preparation for the licensing exams because I was nervous and had the time to study as much as possible. I am not a fan of multiple choice tests as I tend to second guess my answers, so wanted to learn and build my confidence. If I failed, I knew that I could take the test again but who wants to rely on a redo? Not I. My degree is in English Literature and I’d been a stay-at-home mom for 18 years after a brief career in television production. My dad has been a life insurance salesman for over 50 years, but I can’t say I picked up too much from him and felt that I was truly starting from scratch.

I completed online training through WebCE at home in December and January. The basic program worked well for me. You don’t need the extra stuff they offer (workbook, flash cards, etc.) unless you feel like spending more or you prefer paper to a screen.Speaking of, check for a promo code or a coupon for the course. You can go at your own pace and take unlimited practice tests that simulate the exams. The questions are different, but you’ll get a feel for the wording. Much of it is common sense, so learn the basics, vocabulary terms, and focus on state regulations and specific numbers, such as days and dollar amounts. How much is the penalty for breaking a law, how long do you have to change address after moving, in addition to insurance principles.

The courses are 20 hours, which could be more or less depending on the individual. You may start, save progress and return, so long as you finish within the allotted time period (a matter of weeks). You definitely don’t want to have to pay for the course again, so start when you’ll be able to complete it and then you have three months (I think) to take the official exam after completing the precertification. Taking the test as soon as possible, while everything is fresh in your mind, is ideal. I managed to take all four just before COVID-19 wreaked havoc, thankfully.

I heard the classroom sessions are like watching paint dry, but Kaplan offers that option and you may learn better in that environment or want more human interaction. I found that YouTube videos by a man named Lauren Myers were the most helpful for P&C test preparation, actually. He has a way of cutting through the confusion that sticks with you.

Through whichever program you choose, pass the final exam in each division—in my case, Property, Casualty, Life, Accident & Health—and print the certificate(s). Now you’re ready to register for each test at Pearson Vue Testing Center (or a different location). They combine P & C and Accident/Life so you may take two tests back to back (about 30 minutes/120 questions each). Again, check for a promo or a two-for-one deal. You need to score a 70 or above and they will print the result immediately after: Pass/Fail only. The proctor on my test day tried to “Regis” me and act like he was handing me bad news. Not nice!

You should be prepared for a seriously thorough shakedown upon arrival at the testing center. You aren’t strip-searched, but that’s about where it stops. Pockets are emptied, hairstyles are inspected, glasses are checked, mouths opened, and everything you brought with you goes into a locker. Nothing goes into the room with you except your locker key and a provided pad and dry erase marker that is returned and checked after the test. Don’t even think about going to the restroom or else go through the inspection again. The center tests for all sorts of licenses, not just insurance, so they are discriminating. Everyone is equally suspected of trying to cheat.

An applicant who has committed a felony of the first degree, a capital felony, a felony involving money laundering, fraud, or embezzlement, or a felony directly related to the financial services business is permanently barred from applying for a license.

Once you pass, you must apply with your state’s insurance department and pay the applicable fees. Tennessee has a $50 filing fee for each line. You will need to submit to a background check including fingerprinting and await the decision, which for me, meant receiving my certificate in the mail a couple of weeks later. I knew I had a clean background check, but it’s kind of like passing a police cruiser on the interstate, I felt relieved anyway.

My first day of work!

The following is the official general requirements from the state of Tennessee.

An “Insurance Producer” is a person required to be licensed under the laws of Tennessee to Sell, Solicit or Negotiate insurance.

The applicant is at least eighteen (18) years of age.

Resides in Tennessee.

The applicant is competent, trustworthy, financially responsible, and has a good business reputation.

The applicant is required to pass a written examination and complete a prelicensing course of study thru an approved education provider for each line of insurance for which an insurance license is requested. Such course of study must consist of the following minimum number of hours. Approved education providers can be found at Pearsonvue.com. Lines of Insurance / Number of Hours Life / 20 Accident & Health / 20 Property / 20 Casualty / 20 Title / 20 Personal Lines / 20 Application Procedure

Complete prelicensing education requirements through an approved prelicensing education provider for the line(s) of insurance for which you wish to be licensed (Provider will complete prelicensing certification.)

Schedule your examination with PearsonVue. (Phone: (800) 274-4957) You must present your Prelicensing Education Certificate at the exam site on the day of examination.

Fingerprint based background check is required — see attached instructions.

Pass the required examination. PearsonVue will electronically submit your scores to the department.

Submit your application and filing fee ($50.00) to the TN Department of Commerce and Insurance electronically at http://www.nipr.com OR file the paper Uniform Application. YOU MUST WAIT 48 HOURS FROM TAKING THE EXAMINATION TO SUBMIT YOUR APPLICATION ELECTRONICALLY. Processing time for paper applications is 15 days from receipt in the Agent Licensing Section.

You will be issued a license by the Tennessee Department of Commerce and Insurance once you pass your examination and the Department of Commerce and Insurance is satisfied that you meet all other licensing requirements. THE TENNESSEE DEPARTMENT OF COMMERCE AND INSURANCE MAKES THE FINAL DECISION AS TO WHETHER TO LICENSE ANY APPLICANT UNDER TENNESSEE INSURANCE LAW. An insurance producer shall not act as an agent of an insurer unless the insurance producer becomes an appointed agent of that insurer. The appointing insurer shall file within fifteen days from the date the agency contract is executed or the first insurance application is submitted.

Last October 2019, Governor Bill Lee appointed Hodgen Mainda to fill the position left vacant by long-time commissioner, Julie Mix McPeak, who left to work in the public sector in Nashville. Tennessee’s Department of Commerce & Insurance commissioner is appointed by the governor. Most states appoint this post, while ten or so other states elect their state’s commissioner. As we are coming off an election, I got to wondering about this position, so imagine my surprise when I saw the tinge of controversy surrounding the latest appointment and pending resignation.

Hodgen Mainda

Mr. Hodgen submitted his resignation last week and reportedly faces an investigation over allegations of sexual misconduct by one of his department’s employees.

The report of possible sexual harassment was received Sept. 15 and was referred to Lee’s office on Sept. 23.

According to a Department of Commerce and Insurance investigation summary report, there was “insufficient evidence” to substantiate the allegation against Tennessee Department of Commerce and Insurance Commissioner Hodgen Mainda stemming from a February conference in Florida.

Now for a review, just what are the responsibilities of the TDCI Commissioner? In a nutshell, he or she is charged with protecting Tennesseans through balanced oversight of insurance and regulated professions while enhancing consumer advocacy, education, and public safety. The Insurance Division is comprised of seven sections tasked with protecting consumers and ensuring a viable insurance marketplace in the State. This Division regulates and licenses both individuals and corporations, assesses suspicions of fraud, and provides resources to compare various insurance providers for citizens of Tennessee.

As Tennessee’s Commissioner of Commerce and Insurance, Hodgen is the state fire marshal and is responsible for the divisions of insurance, fire prevention, regulatory boards, including twenty-six regulatory entities, TennCare Oversight, and the administratively attached Tennessee Law Enforcement Training Academy, Tennessee Police Officer Standards and Training Commission and Tennessee Emergency Communications Board. In 2018, the department collected $1.145 billion in fees and premium taxes and had expenditures of $220.9 million. [www.tn.gov]

“Today Commissioner Mainda offered his resignation and intent to return to Chattanooga and the private sector,” Ferguson said. “The Governor accepted his resignation.”

Lee’s spokesman Gillum Ferguson

“I have an opportunity to transition to the private sector and at the same time, spend more time with my young family,” Mainda wrote to Lee in his resignation letter on Monday, pledging to make the transition as smooth as possible.

His last day in office is November 13th. Stay tuned for the update when Tennessee’s next Commissioner is announced.

UPDATE from TN.gov—Today Tennessee Governor Bill Lee announced Carter Lawrence will serve in his cabinet as commissioner of the Tennessee Department of Commerce & Insurance, effective immediately.

Carter Lawrence: A lifelong Tennessean and Nashville native, Lawrence earned his Doctor of Jurisprudence and a Master of Business Administration at the University of Tennessee, Knoxville. Prior, he graduated from Wheaton College in Illinois.

Carter is a proven public servant who has stewarded key priorities for the administration throughout his tenure and I’m confident he’ll continue to support TN businesses and consumers with integrity. We appreciate his dedication to @TNCommerceInsur.

A few weeks post-op, I am grateful that I was able to change insurance providers to one that covered the procedure I needed. It wasn’t easy.

Quick backstory: I’ve played tennis my entire life, and my mid-forties knees are feeling it. Last December, an MRI revealed the pain wasn’t going to go away on its own and surgery was necessary to replace the damaged cartilage with donor cartilage. (If I were younger, the doctor could’ve taken my own cartilage from somewhere else, but I’m over 35 or whatever the age cut-off is for a healthy transplant.) As most things medical, the procedure is expensive; the donor tissue alone cost $11,000. Yikes. Turned out, the group insurance my husband had through his employer denied coverage, and come to learn, almost every other carrier would cover it. Unfortunately, we were a couple of weeks past the current plan’s renewal date and were stuck with it. No way could we afford to pay for the surgery without insurance, so I was out of luck.

Until March, when a pharmaceutical company purchased one of the drugs my husband sold and he was technically a new employee, thereby permitted to change his health plan. Six months later, delayed by reasons other than insurance, I finally got to have my knee repaired. Hitting the max out-of-pocket in the last quarter of the year stings a little, but you do what you have to do when you get the chance to do it, right? I have much to learn, yet, but thought I’d share some facts regarding Tennessee Health Insurance since we are coming up on Open Enrollment for 2021.

Open Enrollment is the annual period during which you can enroll in a new health insurance plan for the coming year. If you’re an employee eligible for insurance through your employer, Open Enrollment is the period during which you can sign onto your company’s insurance policy or switch to a different policy. Though you can usually drop your coverage at any point in the year, you may only sign onto a new plan during the Open Enrollment window.

If you find yourself in a position similar to mine, you may qualify for a special enrollment period with a qualifying event, such as:

Changes in your household: marriage or divorce; a new baby or adoption; the death of a spouse in the last 60 days; a significant increase or decrease in salary.

Changes in your residence: moving into a new zip code or from transitional to permanent housing.

Loss of coverage: anyone in the household lost coverage within the past 60 days or anticipates losing coverage in the next 60 days, like a child being removed from a family policy at age 26 when they no longer qualify.

Other qualifying life events: leaving incarceration, gaining residency or citizenship status or gaining membership in a federally-recognized tribe.

When we were looking through all the different options, we had no idea what we were looking for beyond in-network and out-of-network. We had a general understanding of key words, but didn’t know how these terms translated into dollars. Depends on the specific code and charges billed by different providers and is therefore, a bit of a crap shoot, to be blunt. Familiarize yourself with these terms as defined by Benzinga:

A premium is a monthly fee paid to the insurance company to keep your policy active.

You pay out of pocket for a deductible before your insurance coverage kicks in. All insurance plans have different deductibles. A lower deductible means you’ll pay a higher premium each month. Some insurance plans have no deductible at all.

A copay is a flat fee you pay each time you go to the doctor or get a prescription filled. It’s important to note that your copay does not go toward meeting your deductible.

Coinsurance is a percentage that is shared between you and the insurance company. Some common coinsurance amounts:

80/20, where the insurance company pays 80% of the cost and you pay 20%

70/30, where the insurance company pays 70% and you pay 30%

Residents of Tennessee pay an average of $7,372 per year on health insurance, according to the Kaiser Family Foundation. That’s a few hundred dollars below the national average.

from Benzinga.com

It’s helpful to note the following factors will raise your costs, so avoid the ones you can control (diet, exercise, tobacco):

Body mass index: A high body mass index (BMI) can cause certain negative health conditions, including diabetes and heart disease. Insurance companies use BMI as one of the many factors to assess your risk level and how much you’ll pay for insurance.

Tobacco use: Smokers pay more for health insurance. Nearly 23% of Tennessee residents smoke — this is the fourth-highest number in the country.

Age: Older people generally have more health conditions, so you may pay as much as 3 times more if you’re a senior citizen.

Generally speaking, health insurance plans cover treatment for illnesses and injuries but also cover preventive care like health screenings and vaccinations. There’s often no cost associated with preventive services. What’s covered and not covered will depend on your plan, but core benefits are normally the same across all health insurance plans.

What Does Health Insurance Cover?

Ambulance services

Emergency services

Hospitalization

Newborn and maternity care

Prescription drugs

Rehabilitative services

Laboratory services

Mental health care

Wellness checks

Pediatric care

What Does Health Insurance not Cover?

Health insurance covers a majority of the costs associated with the treatment of illnesses or injuries but there are some things that insurance companies do not cover.

Elective or cosmetic procedures, like weight-loss surgery or plastic surgery

Long-term nursing home care

Infertility treatments

LASIK (laser surgery to improve vision)

Alternative therapies

Dental, vision and hearing

As I lay recovering…

Before I go down the rabbit trail of HMOs, PPOs, HSAs and more, I will leave you here and go ice my knee. Be well and take care of yourselves, friends.

Insurance provides peace of mind, even for those worried about alien abduction, but sometimes, if you claim it, you gotta prove it.

I’m sure it’s no surprise to hear that people make some crazy claims to insurance companies and others take out policies for unbelievable coverages. Let’s take a look at a few of the stranger things in the insurance world and how companies might investigate such X-Files.

I recall hearing something about Gene Simmons (from the band KISS) insuring his trademark tongue for millions of dollars in the 70s, and also about Tom Jones insuring his voluptuous chest hair for millions of dollars. Both accounts are cringey, but seem to be true, though no tongues or hairs have reportedly been harmed on either of those fellas.

You can insure just about anything you can put a dollar amount on and where there is a risk of monetary loss to the owner of the policy. While you may think someone else is out of their mind, insurance is partly about peace of mind that allows one to rest a little easier that all may not be lost should tragedy strike. Gene Simmons wore so much make-up, would anyone even recognize him if his serpentine tongue weren’t hanging down past his chin? Did the band’s success truly depend on

iPhone photo taken by me (Katie) at a Panic at the Disco concert with lead singer Brendon Urie playing a piano suspended in air by a cable. Worth the risk?

Brendon Urie’s premium to insure his life and those of his concertgoers must be quite high since he plays a “floating” piano that drifts over his audience. I can’t imagine!

Anything can happen during a concert, festival, or other live event, so it’s important to have liability and property insurance that can handle the unexpected. Large crowds, elaborate sets, and lots of equipment mean risks are ever-present.

from ProSightSpecialty.com

I didn’t mean to get stuck on musicians and concerts; you’re probably wondering what’s with the Parking for Aliens Only sign. One, it’s an attention grabber. Two, policies actually exist for people who are fearful of an alien abduction. A U.K.-based insurer has sold more than 30,000 such policies across Europe. Premiums can cost up to $150 per month for $1.5 million in total coverage, according to projectparanormal.org, which is quite high considering the probability of alien abduction ever occurring. Should one ever make a claim, however, definitive proof is required to collect any damages.

Enter the EUO

An EUO is not related to a UFO, and actually seems scarier to me. The acronym stands for examination under oath and is a formal statement taken by the insured describing the events in the matter of their particular claim. EUOs are typically, although not always, conducted by an attorney representing the insurance company. A court reporter will type every question and answer verbatim, and sometimes a videographer will record the proceedings. Examinations under oath usually last only a few hours, but could possibly extend over multiple days depending on the case. It’s a serious matter.

An insured should anticipate questions about the cause and origin of the loss, the financial condition of the insured leading up to the event (motive), the insured’s whereabouts at the time (opportunity), the nature and extent of the loss, particular items claimed to have been damaged or destroyed, and the accuracy of answers provided in the insurance application. Seeking legal counsel would be a prudent move before undertaking this examination, although an EUO is not part of a court proceeding, anything you say can be used should the claim be taken to litigation and the insurance company may deny the claim based on the results of the investigation.

An insurance company’s authority to take an examination under oath comes from the insurance contract, which typically contains a provision, under the section “Duties of the Insured,” that the insured must answer questions under oath when requested by the insurer. Even without such a provision, there is almost always a “duty of cooperation” provision in the policy which would also require the insured’s participation in an examination under oath. If an insured refuses, it could result in the insurance company’s denial of the claim based on its assertion that the insured breached the insurance policy by refusing to cooperate. See Spears v. Tenn. Farmers Mut. Ins. Co., 300 S.W.3d 671 (Tenn. Ct. App. 2009).

FAQs about EUOs:

Are EUOs always required? Not always. EUOs are often demanded when there are red flags for fraud, strange circumstances, large claims, potential problems with the application for insurance, etc.

What do I need to bring? Bring several documents in support of your claim and be prepared to answer questions about those documents and specific questions about the loss by the attorney.

Do I have to cooperate? Yes. Your insurance policy has a section that provides you, as the insured, have a duty to cooperate with your insurance company’s investigation, including submitting to an examination under oath. However, you may not have to answer every question or provide every document, but it is important to know that you need to cooperate with your insurance company as your failure to do so may result in the denial of your claim.

Do I need an attorney? It would help. An attorney experienced with EUOs can prepare you for the types of questions you will face, assist in the gathering (and presenting) of documentation, streamline and coordinate communication with the insurance company, and assist you in making strategic decisions, all of which can impact whether your claim is paid or denied.

Why am I being investigated? Insurance companies send claims into the examination under oath process for a variety of reasons. Some reasons are serious and legitimate, while others seem to be trivial. You may never know exactly why, but stick to the truth and everything should work out.

Insurance can be confusing–have enough, too much or even need it at all?

I am constantly learning from Cyndi Jeffers, CIC, and thought you might also. She has answered thousands of questions over her 30+ year career, but we don’t have enough time or space to cover them all today. We’ll start with the following 11 points to clear up some common misconceptions about different types of insurance.

PRO TIP: When shopping for insurance coverage, make sure you compare apples to apples. You get what you pay for with insurance, and a lower premium can be an indicator that some of the coverages you had are no longer there, or that the agent didn’t input your information correctly (which could result in denial of a claim).

How much liability insurance coverage do I really need? Purchase enough coverage to protect your assets. If you own a business, and it’s not an LLC or corporation, include the business assets in the total and make sure your business liability is enough to protect your business and personal assets.

When should I add Long Term Care? Long Term Care insurance is not just for the elderly – a bad accident or a debilitating disease can affect a person of any age.

PRO TIP: Take responsibility for maintaining your home. Most things that happen are caused by lack of maintenance, and insurance doesn’t cover that.

PRO TIP: Drive defensively – don’t assume the other driver knows what they’re doing. Most auto accidents are caused by distracted drivers.

What’s the difference between Market Value and Tax Appraisal? Property insurance is not based on market value or tax appraisal. Market value is a reflection of what someone is willing to pay for a property; tax appraisal is typically based on market value, a set millage rate, and a tax rate. Neither market value or tax appraisal are good indicators of what it would cost to rebuild your home or business building as it stands now – that’s what insurance is for.

A millage rate is the tax rate used to calculate local property taxes. It represents the amount per every $1,000 of a property’s assessed value. Assigned millage rates are multiplied by the total taxable value of the property in order to arrive at the property taxes.

from investopedia.com

When should I contact my agent? Major changes should always be reported to your agent! It’s not about possibly raising your premium – it’s about continuing to pay premium for a policy that may no longer fit the situation and therefore may not provide coverage in the event of a loss.

Can I use my personal auto insurance for my company vehicle? If you use a personal vehicle for business, be sure your agent is aware of it – there is only limited coverage for business use on a personal auto policy. If you have an advertising sign on your vehicle or you have employees who drive your vehicle, it’s time for a commercial auto policy.

I just wrecked my car. Who do I call first? Before you call the 800 number to file a claim, contact your agent to discuss what happened. People often panic and call the insurance company, setting up a chargeable claim when maybe the damage is less than the deductible, the other person’s insurance is responsible, or you find it’s a maintenance issue not covered by insurance. Your agent is there to help you!

Can I change the type of roof on my house that was damaged by a storm? The basic purpose of insurance is to put things back the way they were before the loss occurred – it’s not meant to provide additional benefits. If you didn’t have a metal roof on your home before the hail storm, you will not have one after the claim is settled (unless you pay the additional cost yourself).

PRO TIP:If you know of someone who committed insurance fraud, report them – their actions are affecting everyone, including you!

Insurance fraud is a major factor in insurance premium increases. Property & casualty insurance companies lose approximately $34 billion a year to insurance fraud, while as much as $259 billion was paid out as a result of healthcare fraud in 2010 alone. In addition, the cost of combating fraud is also passed on to the consumer. Insurance fraud takes many forms and is committed by insureds, contractors, healthcare professionals, etc.

It’s best to secure a life insurance policy when you’re relatively young and healthy.

My husband and I purchased a term life insurance policy 18 years ago, shortly after the birth of our first child. I’m not sure we would have thought to buy if my father had not been an insurance salesman; nonetheless, we felt like responsible parents. All I knew is that it was fairly inexpensive and that I hoped we would never use it. Thinking about your own death or losing a loved one is not on anyone’s wish list, but you know what they say about death and taxes–it’s inevitable.

Securing a life insurance policy when you’re relatively young and healthy is ideal if you are responsible for other people and have the resources. If you are on your own, there’s really no point. When it comes to how much coverage you should carry, experts recommend a sum that is 10-15x your income. That’s likely a high number, but you can imagine how quickly that number will shrink when bills are due and life goes on. Ask yourself three questions:

Who depends on me?

How much can I afford?

How healthy am I?

Many companies offer life insurance to their employees, and that’s great, but it is usually insufficient for anyone who has other people depending on them for daily living expenses for an indeterminate period of time, such as a spouse, sibling or elderly parent. What about the mortgage, car payments, private school or college tuition, or possibly a wedding in the near or distant future? Basically, the more responsibilities you have, the more coverage you need.

My parents, Tom and Sandy, with their daughters, sons-in-law and grandchildren to celebrate their 50th wedding anniversary in 2013. Families sure can grow!

Talk to your agent about the different options of term, whole, and universal life policies to determine which would best meet your needs now and fulfill the needs of your dependents later.

Your financial and family situation will determine whether you need life insurance.

The younger you are the lower your premiums, but older people can still get life insurance.

Carry as much as you need to pay off your debts plus any interest.

Your policy’s payout should be large enough to replace your income plus a little to hedge against inflation.

from Investopedia

While we’re on the subject, I thought it would be fun (in a macabre sort of way) to share the lifetime odds of death for selected causes. The world is battling a pandemic at the moment thanks to COVID-19, so mortality and the fragility of life is on the forefront of every news report and social media post. Here are some statistics for other ways to die from the U.S. National Safety Council, based on data from the National Center for Health Statistics, 2017.

The more your boat is worth, the more important insurance becomes to protect yourself from financial loss.

You can’t buy happiness. But you can buy a boat and that’s about the same thing.

Too many sources to credit

In East Tennessee, our lakes are usually crowded with teenagers jet-skiing, fishermen fishing, friends sailing, families cruising and debris floating. After the deluge of rain this past spring, boats and skiers are still dodging flotsam and jetsam throughout the river. Most boaters know that sinking feeling when a propeller wrestles with a log, but did you know that boat protection can help cover the cost of repairs? If you have comprehensive insurance or property damage coverage built into your watercraft policy, your boat insurance will cover collision with rocks, logs, and other marine obstacles.

It’s not like I own a yacht, why would I need a watercraft policy?

The amount of boat insurance you need depends on a number of factors, including the boat’s value, motor size, age, and how it’s used. In general, most professionals recommend buying at least $1,000,000 in liability insurance, with boat insurance ranging anywhere from as little as $75 to as much as $500 per year. For uninsured/underinsured motorists coverage, a typical minimum is $10,000 to cover losses in the event someone without insurance is at fault in an incident on the water. The amount you purchase is flexible and should reflect the potential injuries you may incur if you or one of your passengers is seriously hurt, or your vessel is damaged. For example, a brand new high performance speed boat will need more coverage for bodily injury and property damage liability than a low-risk, slow-moving pontoon.

Boater’s insurance typically covers:

Collision damage: Covers repairs or replacement in the event that your boat is damaged in an accident.

Property damage liability: Should you damage someone else’s boat or property, then this will keep you covered.

Bodily injury liability: In the event that you should injure someone while operating your boat, this helps protect your assets.

Comprehensive: If your boat is stolen, vandalized, or damaged in a non-collision manner, your comprehensive provides compensation.

Men have a tendency to forget their age on the water and take all sorts of risks.

In the event that your boat’s wake causes damage to another watercraft or capsizes another boat, you would be responsible and could be held liable for damages. Don’t be caught off-guard, take out a boat insurance policy.

So, what does my Homeowner’s policy cover?

A home insurance policy provides limited coverage for your boat or watercraft should it be damaged, stolen or vandalized. In most policies, you would only be reimbursed up to $1,000 worth of coverage if your boat, jet ski or miscellaneous water craft is broken or damaged by the following: fire, wind, explosion, hail, theft, vandalism or falling objects. Since homeowner’s policies can have deductibles either greater than or close to $1,000, most claims would not make sense to file.

When it comes to hail damage, there is a peculiar provision in which the watercraft must be in an enclosed building for the damage to qualify. For example, if a hailstorm causes damage to a boat stored outside, you wouldn’t be able to file a homeowners claim in that case. But if the building or storage enclosure has glass that gets shattered and hail comes through that damages your boat, then you would be covered.

Personal Property

If you have items on your boat that are stolen or destroyed, you can likely use your homeowner’s insurance to recoup those losses. For example, your homeowner’s policy would cover your portable Bose speaker, but high-priced modifications and equipment exclusive to your boat should be covered under a boat insurance policy. Therefore, always carefully review the comprehensive coverage of your policy to determine exactly what is and is not covered. You may need to purchase additional riders, or policy endorsements.

Captains and vessels come in all sizes.

If you injure someone or damage property with your watercraft, the homeowner’s liability policy can help cover any associated cost. These policies come with at least $100,000 in liability coverage you can use for legal expenses or restitution to pay the affected party. There are some important size and horsepower limitations when it comes to boats however. Generally the boat needs to be very small, and in no case will your jet ski be covered. To get more robust coverage for your boat or watercraft you should take out a boat or personal water craft (PWC) insurance policy.

Vessel/Motor Type

When is it Covered by Liability Insurance?

Inboard or Inboard-Outdrive

Less than 50 HP

Outboard

Less than 25 HP

Sailboat

Smaller than 26 feet

Jet Skis

Never

Air boats

Never

From valuepenguin.com

Whether you’re spending every day on the water or have your boat in storage for the winter, it’s important to keep your watercraft protected against the unexpected year-round. Coverage is not required by law, with the exception of Arkansas and Utah, but your lien holder and/or marina where you dock may have requirements. An agent can help answer your questions, but you can also learn about the coverage types below:

Watercraft medical payments coverage Helps pay medical costs if you or anyone on your boat is injured in an accident.

Watercraft liability coverage If there’s an accident, this covers the medical and other expenses of whoever was injured as well as the costs of repairing or replacing another person’s boat or property.

Property coverage Covers the damage to your boat if you’re involved in an accident with another boat or something else, like a pier, buoy, dock or debris. It also typically pays for damage caused by something other than a collision, such as theft, fire or vandalism.

Repair cost Covers the repair work done on your boat, motor, equipment or trailer with no deduction for depreciation*.

Emergency services If your boat breaks down, this covers the cost of towing and labor and the cost of delivering fuel, oil or a battery.

Uninsured watercraft coverage If you’re in an accident with an uninsured boater, this helps pay for injuries that you, your family or anyone else on your boat sustains.

Agreed value option When you’re reimbursed for your boat’s value, you’ll be reimbursed for what it was worth at the start of the policy regardless of the current market value.

Personal effect coverage Covers your fishing equipment and other personal belongings if they’re damaged, lost or stolen.

Additional boat equipment Covers boat accessories, like anchors, life jackets and navigation gear, up to the policy limits.

Boat trailer coverage Covers damages to your trailer resulting from an accident or other unforeseen incident.

Lying on your insurance application is never okay.

You may be wondering: What’s the clue, then?

C.L.U.E. is also known as a Loss History Report and reports an insured’s history of claims and losses on their home or auto within seven years from the date of the request. Each month, participating homeowners and auto insurance companies report claims history information, which goes into a central database called the Comprehensive Loss Underwriting Exchange (C.L.U.E.). How is knowing this good for you? One: you can order your own report to verify its accuracy and keep track of your records. Two: the report is used by insurers to help prevent fraud when applicants fudge their record and mess with the fluctuation of premiums.

Under the Fair and Accurate Credit Transaction Act (known as FACT or FACTA), you are entitled to receive one free C.L.U.E. Auto and C.L.U.E. Personal Property report every 12 months.More than one will cost $19.95.

C.L.U.E. Reports are linked to the individual, not the property or car, so it only includes the history of personal property or auto insurance losses of a single owner, and only information concerning the insurance policy.

What’s in the report?

The name of the insurance company

The date of any losses and claims

The type of loss—fire, wind damage, etc.

Whether or not the claim was denied

If not denied, the amount that the insurer paid out

The homeowner’s insurance policy number and claim number

What’s not in the report?

Legal judgments

Criminal records

Civil lawsuits

Credit reports

Information from any state department (i.e. DMV) or a similar organization

Sensitive or private information, such as a Social Security number or credit card information

If you find any inaccuracies on your home’s C.L.U.E. report, you can contact LexisNexis to resolve the dispute at 888-497-0011, by email at consumer.documents@LexisNexis.com, or by postal mail at LexisNexis Consumer Center, ATTN: FACT Act Dispute Request, P.O. Box 105108, Atlanta, GA, 30348.

We get it. You’ve made mistakes–we all have–but do not compound your troubles by lying on your insurance application. I remember, as a new mom, answering questions on the life insurance form and my husband being so frustrated with me because I took each question seriously. Signing a legal document strikes a fear in me not unlike swearing on the Bible to tell the whole truth and nothing but the truth. It baffles me that people can outright lie, though I also haven’t been in a situation where my life or a great deal of money depended on it, so judge not and all… but, in the matter of insurance, other people’s lives and a great deal of money do depend on telling the truth. Withholding information or intentionally making misrepresentations is fraud.

“Taking creative liberties on your insurance application may seem like an innocent white lie, but it’s actually considered fraud, and the repercussions can be serious. If found out you may be charged a higher premium, denied a policy or even charged with fraud, requiring you to pay a fine or even do jail time.”

Finder’s consumer advocate Rachel Dix- Kessler.

The nice folks at insurancehotline.com listed six possible consequences of being dishonest with your insurance company:

1. Your insurance policy could be cancelled

If your policy is cancelled, you’ll likely have to pay more to get a new policy elsewhere. Policy cancellation for non-disclosure puts you in a high-risk category. Being in a high-risk insurance category automatically makes it harder for you to get new insurance.

2. Your claim will be denied

Let’s say you tell your insurance company that you don’t drive your car to work every day, but you really have a 50-kilometre commute each way. If you’re in an accident while on the commute, the company may deny your claim because you didn’t tell them the truth about your daily driving.

3. Your insurance premiums will go up

Insurance companies provide policies and charge premiums based on the information you, ideally, truthfully provide. If you drive a lot or have had accidents in the past, this increases your risk for a future accident. If you didn’t disclose problems in the past and the company learns of them, your premiums will go up, because the company will have a more accurate picture of your potential risk.

4. You could be denied car insurance in the future

When you’re dishonest with your car insurance company and they discover it, whether it’s because of a claim you make or other means, it’s more serious than if you told the company from the beginning that you’d had an accident or tickets.

The insurer is within its rights to deny your car insurance in the future.

5. You could face fines and penalties

You may have to pay money to your insurance company or receive a fine under your province’s insurance regulations. The amounts vary, but if a claim was paid under fraudulent circumstances, you could be held financially responsible for it. An insurance company can sue you to recover costs and damages under Canadian law.

6. You could face criminal penalties

A false insurance claim can lead to jail, substantial fines, and a permanent criminal record.

Common Omissions (from Investopedia)

These may result in a lost policy, inability to get new coverage, fines, a legal order to pay back premiums—or even jail time. Do not try this at home.

Accidents or tickets

This is the easiest thing for insurers to look up, regardless of what state you live in. The fender bender you sustained on the West Coast did not vanish from databases when you moved to New Jersey. Although that speeding ticket you got may seem like ancient history, the insurance carrier isn’t likely to sympathize.

The primary driver

Typically, this involves a parent claiming to be the one who uses the insured car the most, when in reality it is his college-age son. Young men have high premiums because they get in more accidents and are bigger risks.

The number of miles you drive

The more time a car spends on the road, the greater the likelihood it will be involved in an accident. Often, a motorist will claim the daily commute is shorter than it really is. That can make explaining what happened more difficult when you smash up the auto a greater distance from home.

How you use the car

Let’s say you use your car for work—delivering pizzas or hauling tools to make home repairs. But you tell the insurer that the vehicle is solely for shopping and recreation. When you get in a wreck on the interstate and the police report notes the dozens of pizza pies splattered all over the car’s interior, it doesn’t look good to the insurance company investigating your claim.

Where you actually live

If your home is in a high-crime area or big city, you might be inclined to list your sister’s address as yours. She lives in a peaceful suburb, which statistics show has a lower chance of a car being stolen or damaged. That lie is very easy to disprove.

Some 35 million Americans say they’ve played fast and loose with the facts when applying for insurance, with a whopping 6.5 million (29%) of these lies told on car insurance applications. Health insurance fibs take second place at 6 million (27%) lies, followed by life insurance at 3.2 million (14%).

Type of insurance

% of lies

Estimated total insurance lies

Car insurance

29.30%

6,518,166

Disability insurance

5.10%

1,133,594

Health insurance

27.39%

6,093,068

Home insurance

11.46%

2,550,587

Income protection

3.18%

708,496

Life insurance

14.65%

3,259,083

Pet insurance

3.18%

708,496

Renters insurance

2.55%

566,797

Travel insurance

3.18%

708,496

Statistics from finder.com 2018

Now that you know what’s good for you, don’t be CLUEless.

Full coverage does not mean everything is fully covered if you were to wreck your car or have an accident. It is a package term used to describe a combination of comprehensive, collision and liability coverage within one policy.

Comprehensive Coverage is also referred to as Other-than-Collision because it covers your vehicle if stolen, vandalized, set on fire, and other random things that don’t involve running into another object and are outside of the driver’s control.

Collision Coverage includes a fender bender or running into a telephone pole or fence. It helps pay for the cost of repairing or replacing your vehicle up to the actual cash value if you run into another vehicle, a snowbank, or an object in or on the ground (such as a guard rail or roadkill).

Liability Insurance helps pay the expenses the other driver incurs if you are found at fault for an accident.

Full Coverage does not exist.

Tennessee requires that car insurance policies include, at a minimum, the following coverage limits:

Bodily injury liability: $25,000 per person and $50,000 per accident

Property damage liability: $15,000 per accident

REMEMBER:

Automobile liability insurance is financial protection for an at-fault driver who harms someone else or their property in a car accident.

Bodily injury liability helps cover medical expenses for those involved in the accident.

Property damage liability helps cover costs of repairing the vehicles of the other drivers involved in the accident.

Other important coverages to consider:

Medical Payments Coverage–regardless of who’s at fault, this covers medical bills for you and any passengers in your car if injured in an accident.

Uninsured/Underinsured Motorist Coverages (UM/UIM)–designed to protect you and your vehicle if someone hits you and either doesn’t have insurance or not enough insurance to cover the costs.

Custom Parts & Equipment Coverage–protection for after-market upgrades to your car, including a sound system or custom grill. Your standard collision and comprehensive coverages may not cover upgrades that were not factory-installed.

Rental Car Coverage–this covers the cost of a rental car while yours is in the shop after a covered incident.

Loan/Lease Gap Coverage–this coverage can help cover the remaining balance you may owe on your loan or lease (up to an increase of 25% of your car’s actual cash value).

Emergency Roadside Assistance (Towing/Labor) Coverage–This coverage is there to help when your car breaks down, you have a flat tire, or you run out of gas. Emergency roadside assistance covers up to $75 per incident.

Speak with your agent to determine how much coverage you have and how much coverage you need.

We will make sure you aren’t fooled by full coverage claims.