Herron-Connell Covering the Details of Tennessee Insurance

Author: Kate Rymer

I am a second-year licensed independent agent at Herron-Connell Insurance Group in Oak Ridge, TN. I love to learn about all facets of insurance, specifically in Tennessee.

The Underwriter wants to know everything about you — let’s learn more about them.

The Who

Insurance underwriters are trained to identify, understand and prevent risks in either life, health, or property and casualty insurance. Property and casualty is a broad field that can include business, home or auto insurance. Their specialized risk assessment knowledge enables them to determine whether they will insure something or someone and for how much. Underwriters decide whether to agree to be financially responsible to the insured if something unexpected or catastrophic happens related to the policy.

So, the underwriter decides if you are worth a monetary risk to cover you and how much premium will be charged if approved.

The What

The U.S. Bureau of Labor Statistics describes what an underwriter does as follows:

Analyzing insurance applications

Identifying the risks of insuring applicants

Screening applicants based on a specific set of criteria

Evaluating recommendations from underwriting software

Contacting field representatives, healthcare providers, and others for more data

Deciding whether to offer insurance

Determining appropriate premiums and amounts of coverage

Reviewing and updating the rules for automation software

The difference between the specialties lies in the criteria used to make the decision. For life insurance, examples of the criteria are age and financial history. For health, the main criteria are medical history and age. For auto insurance, underwriters look at driving record, age and type of vehicle. In everything they do, insurance underwriters must strike a balance between risk and caution. Too much risk means the insurance company will pay out too many claims. Too much caution and the carrier will not make enough money from premiums.

The Where

Underwriters work for insurance companies and can usually be found at desk in the company headquarters or a regional office. They use software systems to analyze and rate insurance applications, make recommendations based on risk, and adjust premium rates according to the risk. Sometimes they might work overtime or on weekends, depending on the type of underwriting, and they may inspect the property or vehicle in person. The average salary has been on the rise over the years and depends upon qualifications, education, experience and location.

The How

Insurance underwriters use a software program to recommend coverage and premiums based on the specific data provided by the applicant, and will approve or reject the application after an evaluation of the software results. For simple and common types of policies, such as those for automobile or homeowners’ insurance, the automated recommendations are commonly followed.

For more complicated types of insurance, such as workers’ compensation or business income, underwriters rely on analytical insight and experience. For example, in some cases, a reported bankruptcy or cancer treatment might impact a policy so they will review other sources such as medical records and credit scores.

The How To (become an underwriter)

{from kaplanfinancial.com}

“In general, to become an insurance underwriter, you should have excellent decision-making and mathematical skills, strong analytical and computer skills, and good interpersonal skills. You should also be detail-oriented. You’ll need a bachelor’s degree at a minimum. You do not have to be a finance or business major; however, you should plan to complete mathematics, economics, finance, and business courses. Unlike insurance agents and financial representatives who sell insurance as an investment, you do not have to have a license to become an underwriter. However, in some of the larger insurers, having an insurance license can help you stand out in a group of prospective trainees or associates.

Underwriters who are just starting out are usually required to be an associate for an established underwriter, learning about basic applications and common risk factors on the job. As they become more experienced, they begin to work more independently, and their work becomes more complex. Also, big insurance firms often offer comprehensive training for new hires. Eventually, they no longer need supervision and will work independently as underwriters. Most underwriters participate in underwriting professional development to sharpen their skills and knowledge.”

The Why

The role of an insurance underwriter includes responsibilities such as:

Evaluating information about the potential client (i.e., age, marital status, medical history, driving record, etc.)

Using underwriting software to analyze the risk profile of the potential client

Deciding whether or not insurance coverage should be offered to an individual

Calculating costs to provide coverage and establish the pricing for the premium

Developing solutions to reduce the risk of paying future insurance claims

Analyzing actuarial tables, which is the data provided by actuaries

Although some of the work is automated and is carried out by insurance software, as mentioned above, an underwriter will still be involved with a potential client if a change in risks or change in the conditions of the insurance policy is likely. The underwriter will determine whether or not the insurance company would like to continue with providing insurance coverage or if it will establish new insurance terms with the client.

The End, but actually the beginning

The term underwriter first emerged in the early days of marine insurance. Shipowners sought insurance for a ship and its cargo to protect themselves if the boat and its contents were lost. Shipowners would prepare a document that described their ship, its contents, crew, and destination and go to the local hangout or pub, usually.

An agreed-upon rate and terms were set out in the paper. Business people who wished to assume some obligation or risk would sign their name at the bottom and indicate how much exposure ($) they were willing to accept. These businessmen became known as underwriters. They would get a return on their investment or help cover the loss in the event of an accident.

This post is for the intrepid traveler daring to leave their house.

Disclosure: I’ve never purchased travel insurance. I almost did when I took my daughter to NYC for her 18th birthday in 2020–January, mind you–but I made sure the arrangements were all refundable by a certain date. The fact that the city shut down less than two months later because of a pandemic would have been unimaginable, and has prompted travelers to take precautions they might not have otherwise. Here’s a primer on travel insurance.

I was more concerned about weather delays in NYC January 17-19, 2020.

Travel insurance is coverage designed to protect against risks and financial losses that could happen while traveling–from minor inconveniences like missed airline connections and delayed luggage to more serious issues including injuries or major illness. As we know, Covid-19 has shoved the elephant out of the room, so I’ll begin with FAQ regarding travel insurance coverage and cancellation for illness.

Does Travel Insurance Cover the Coronavirus Pandemic?

On January 21, 2020, the Coronavirus disease 2019 (COVID-19) became a named event, which affects the travel insurance coverage available for new policies purchased thereafter because it is known. Insurance is designed to protect you from an unpredictable or spontaneous loss. For example, if a hurricane ruins your trip, travel insurance would only cover you if you bought it before the hurricane formed. Be sure to purchase insurance as early as possible and always read the fine print no matter what policy you choose.

Comprehensive travel insurance

This is the typical policy that people imagine when they think of trip insurance. The comprehensive policy usually covers delays, cancellation due to sickness or death, lost luggage and some emergency medical costs.

Benefits included in comprehensive coverage may apply in the following unforeseen scenarios:

Emergency Medical Coverage: a sick traveler must see a doctor and/or go to the hospital during a trip.

Emergency Medical Evacuation Coverage: in rare cases, a sick traveler requires an emergency medical evacuation to the nearest appropriate hospital or back home for recuperation.

Trip Interruption: an extremely sick traveler cannot continue with a trip and must return home.

Cancel For Any Reason: Currently, if you are looking for trip cancellation coverage because you are concerned about the coronavirus, you will now need to purchase a plan that includes Cancel For Any Reason since the travel warnings are now foreseen. This benefit is time-sensitive and has other eligibility requirements, so not all travelers will qualify.

Some plans may exclude epidemics/pandemics and may not provide coverage for related issues. Please be sure to read the plan details carefully before purchasing.

Over the course of the coronavirus pandemic, many traditional travel insurance companies have expanded or adapted their existing coverage for travelers. In addition to the coverages above, examples of these may include:

Reimbursement for covered medical treatment during a trip due to a COVID-19 illness

Get sick with COVID-19 and must cancel a trip by physician’s order

Physician orders a quarantine before trip

Lost a job during the coronavirus pandemic by no-fault of your own

Cancel For Any Reason (CFAR) offers the most trip cancellation flexibility and is the only option available to cover fear of travel. CFAR is an optional, time-sensitive benefit with eligibility requirements, so not all travelers will qualify. Full terms of coverage will be listed in state-specific policy. If eligibility requirements are met, reimbursement is up to 50%-70% of the insured prepaid non-refundable trip cost.

InsureMyTrip.com

Does Emergency Medical Coverage Travel with You?

Some travel insurance plans do offer emergency medical benefits if you need a doctor or hospital visit during a trip. Check your personal health insurance plan first to understand coverage already in place. However, most health insurance plans don’t provide full coverage in foreign countries and some health plans provide no coverage at all. Travel insurance works in addition to your everyday health insurance and can help supplement medical costs if you get sick or injured before or during your vacation.

If you have Medicare or Medicaid, be aware that medical costs overseas are generally not covered.

Before purchasing a policy, it is imperative to read the policy provisions to see what exclusions apply, such as preexisting medical conditions, and do not assume that the new coverage mirrors that of an existing plan.

Emergency medical coverage may be redundant. Most health insurance companies pay “customary and reasonable” hospital costs if you become sick or injured while traveling, but few will pay for a medical evacuation.

From InsureMyTrip.com, medical plans and coverage to consider include:

Travel Medical Insurance is offered either as part of comprehensive travel insurance plans or can be purchased as a stand-alone plan. These plans only offer coverage while traveling outside of your home country. Contact your regular health insurance provider to inquire about global benefits and how your benefits apply when you are outside of your home country.

Emergency Medical Evacuation Coverage provides transport assistance in the event that you become seriously ill or injured while traveling. Generally, these plans provide emergency medical evacuation to the nearest appropriate care facility if the assistance company and the physician feel you’d be better suited at a different facility. For those who want to ensure transport to the hospital of their choice, travelers may want to consider also purchasing an air medical transport membership. If hospitalized during your trip, this membership may provide transport to a hospital of your choice, often closer to home, without it being determined as “medically necessary” as required on typical travel insurance plans. (For medical transport memberships, some destination restrictions may apply for evacuations related to COVID-19.)

Trip Interruption Coverage is included in travel insurance comprehensive plans. It’s a benefit that offers travelers reimbursement of their pre-paid, non-refundable expenses should they unexpectedly need to cut their travels short. However, there are exclusions for this, so be sure to review your policy carefully.

Travel insurance can help cover expenses stemming from lost or stolen luggage. This is especially useful if an airline loses your bags, as it can be very difficult to get them to pay for lost luggage. In the United States, the Department of Transportation (DOT) requires airlines to compensate fliers up to $3,300 for lost baggage. In foreign countries that amount is a maximum of $1,750. But to receive those maximum amounts, passengers must provide receipts proving the value of the lost bags and their contents. And some airlines require that the claim be filed within 21 days.

To make matter worse, DOT doesn’t define when baggage is officially lost (as opposed to just “delayed”). Overseas, a bag is only considered “lost” after 21 days. For delayed bags, DOT only requires airlines to provide victims with enough money to buy necessities like clothing, medicine and toiletries.

The possibility of baggage and personal belongings being lost, stolen, or damaged is a frequent travel problem. Many travel insurance policies pay for belongings only after you exhaust all other available claims. Your homeowners or renters insurance may extend coverage outside of your domicile, and airlines and cruise lines are responsible for loss and damage to your baggage during transport. Also, credit cards may provide automatic protection for things like delays and baggage or rental car accidents if used for deposits or other trip-related expenses.

What if. . . Plans Change

Travel insurance can help cover costs stemming from trip cancellations. Most resorts or cruise lines won’t give you a full refund in the event of a cancellation. If you cancel two weeks or more before your trip, most resorts will at least charge a cancellation fee; many cruise lines might only give you a 25% refund or will give you partial credit on another cruise. If you cancel within two weeks of a trip, with most companies you won’t give any refund whatsoever. Unforeseen circumstances happen, and you want to be covered just in case.

Before looking into travel insurance, think about the reasons you might cancel. Is a trip delay due to weather going to dramatically change your vacation? Is it possible your school year will be extended, or you will need to take a work-related trip instead? Are there acts of war in the country you’re going to visit? Are you nervous about the CDC issuing a travel warning for your vacation destination?

These are all valid reasons, but not all travel insurance covers these concerns. When booking a pricey trip, investigate insurance at the same time. Some policies require you buy travel insurance within a certain amount of time after making your initial trip payment, such as within 10 to 30 days.

Purchasing Travel Insurance

Travel insurance will vary by the provider on cost, exclusions, and coverage. Be sure to read all disclosure statements and check what protections your credit card might offer.

Coverage is available for single, multiple, and yearly travel. Per-trip coverage protects a single trip and is ideal for people who travel occasionally. Multi-trip coverage protects numerous trips occurring in one year, but none of the excursions can exceed 30 days. Annual coverage is for frequent travelers. It protects for a full year.

Premiums are based on the type of coverage provided, a traveler’s age, the destination, the duration, and the cost of your trip. Standard per-trip policies cost between 4% to 10% of the trip’s cost. Specialized policy riders focus on the needs of business travelers, athletes, and expatriates (i.e. working overseas).

Also, it is suggested that a traveler register travel plans with the State Department through its free travel registration website. The nearest embassy or consulate can contact them if there is a family, state or national emergency.

Worthy travel insurance plans always include the following provisions:

Coverage for most countries in the world (including the places you plan on visiting).

Some coverage for your electronics (and have the option for a higher coverage limit).

Coverage for injury and sudden illnesses.

Offer 24/7 assistance (you don’t want to call to be told to call back later).

Coverage for lost, damaged, or stolen possessions like jewelry, baggage, documents, etc.

Coverage for cancellations for hotels, flights, and other transportation bookings if you have a sudden illness, death in the family, or some other emergency.

Coverage for political emergencies, natural disasters, or strife in the country that cause you to head home early.

Financial protection if any company you are using goes bankrupt and you are stuck in another country.

Recommended online agencies for the best service and value are:

Just as important as knowing what your plan covers is knowing what it doesn’t cover. Generally speaking, most plans don’t cover:

Accidents sustained while participating in extreme adventure activities such as hang gliding, paragliding, or bungee jumping (unless you pay for extra coverage).

Alcohol- or drug-related incidents.

Carelessness in handling your possessions and baggage.

Recklessness (how “reckless” is defined is a matter up to each company).

Pre-existing conditions or general check-ups. For example, if you have diabetes and need to buy more insulin, you won’t be covered. If you want to go see a doctor for a general check-up, you aren’t covered either.

Lost or stolen cash.

Your theft coverage won’t cover you if you left something in plain sight or unattended.

If civil unrest makes your destination unsafe but your government hasn’t called for an evacuation, you’re probably out of luck too.

Options to include:

Payment for expenses if you get sick or injured on a trip

Travel medical and accident coverage

To be taken to the nearest hospital or flown home if necessary

Emergency evacuation and repatriation

Reimbursement if you get sick and have to cancel or end your trip early

Trip cancellation AND trip interruption

Payment for lost, stolen or damaged luggage or goods

I believe travel is good for the soul, and travel insurance is good for peace of mind. Look into the options, talk to your agent, and decide whether it’s worth it to you.

A weatherized home will be healthier, safer and more energy efficient. Here’s why and how to do it.

Every winter, school-aged Tennesseans (and weary teachers) pray for enough snow to cancel school. They have tricks, like flushing an ice cube and sleeping in pjs turned inside-out, in hopes that the snow will stick. Some areas in the mountains have accumulation, but we here in the valley don’t see much; rather, the snow quickly melts upon landing. When school is canceled, usually the danger is from black ice and most lawns are clear by the afternoon, so we don’t have a typical winter filled with snow. The effects of harsh weather can accumulate despite what we see. Keep reading to find out the benefits of and instructions for weatherizing your home. Note: all seasons contribute to the wear and tear of a home and your health.

Tennessee has all four seasons – winter, spring, summer and fall – each with different weather conditions.

weatherization benefits your health

Weatherization can maintain or improve respiratory health, mental health, physical safety and wellness. Managing a steady temperature improves indoor air quality and benefits everyone. Homes that get too cold in the winter or too warm in the summer increase the risk that residents will develop illness and increase the number of visits to the doctor or hospital. Poor indoor air quality or asthma triggers increase the risk of illness, so people with preexisting medical conditions like asthma, emphysema or COPD will likely benefit even more.

How do I know if my home is weatherized?

If you have to ask, it probably isn’t but here are some ways to know. Do you feel comfortable at home? If you are experiencing unmanageable temperatures, uncomfortable indoor air conditions, or excess moisture in your home, you will likely benefit from weatherization. Some other things to look for are moisture condensed between the glass panels of a window; a furnace that cannot maintain a comfortable indoor temperature; a drafty door or window; a leaky roof.

Air sealing, insulation, moisture control and ventilation are all types of weatherization. The US Department of Energy (DOE) has recommendations for these four topics:

Do: One of the first things you should do is schedule a furnace inspection. Whether you have forced hot air or hot water baseboard/radiators, it’s always a good idea to have your furnace or boiler inspected and serviced before the winter months arrive. When you do so, make sure you are hiring an HVAC professional to do the work. If you have forced hot air heat, this is also a good time to have your ducts cleaned. Stocking up on filters so that you can change them monthly is a good idea. If you have not done so already, consider switching to a programmable thermostat, which can add up to big savings once the cold weather hits.

Don’t: You shouldn’t wait until the first cold night to turn on your furnace. That’s when you will actually need it. It’s best to test it prior to needing it. Also, don’t attempt to service your furnace yourself. If the cold weather has arrived and you will be going away for a short time, don’t turn the heating system off. It’s best to just turn it down to a minimum temperature of 50° or so. That way you will ensure that nothing will freeze while you’re gone.

The dangers of winter come in many forms.

Do: Take a walk around the outside of your home. Keep an eye out for cracks in your homes foundation and repair them immediately if found. Also, clean out your gutters and downspouts. This will keep debris from trapping moisture, which can freeze, buildup and damage your gutters, roof and siding.

Don’t: Leaving hoses connected to the outside of the house can cause damage to your plumbing. Make sure that hoses are disconnected and they are drained completely. If you have outside AC units, don’t cover them with plastic as it could cause damage to them over the winter.

Do: Have your chimney inspected and cleaned if necessary. If you don’t have one already, get a cap or screen installed on the top of your chimney to keep out rodents and birds. If you have a fireplace, inspect the damper to make sure it opens and closes properly.

Don’t: Don’t just hire anybody to clean your chimney. Make sure that they are a certified chimney sweep. The Chimney Safety Institute of America (CSIA) has resources available to help you to learn more. Make sure that you do not store your firewood next to the home. This can attract bugs and rodents.

Do: Inspect your windows and doors for gaps. Add weatherstripping and insulation where appropriate. If you have summer screens in your basement windows, replace them with their glass counterparts for the winter. Check your attic for adequate insulation levels and add more as needed.

Don’t: Be careful not to over-insulate your attic. Often, insulation can be packed too tightly, which reduces its R-value. In addition be careful not to clog the vents at the eaves, reducing airflow and resulting in issues down the road.

[The above text is from Christmas Lumber.]

the benefits of weatherization

According to the Oak Ridge Institute for Science and Education, after a home weatherization residents note additional benefits related to health and finances:

Reduced Carbon Monoxide Poisonings

Reduced Home Fires

Reduced Thermal Stress on Occupants

Reduced Asthma-Related Medical Care and Costs

Increased Productivity at Work & Home Due to Improvements in Sleep

Fewer Missed Days at Work

Reduced Use of High Interest, Short-Term Loans

Increased Ability to Afford Prescriptions

Reduced Need for Food Assistance

assistance with weatherization

Contact your energy provider. Many utility companies have websites, newsletters and in-home services to help their customers understand energy consumption and weatherization. Some utilities will even offer an energy audit and provide information for the U.S. Department of Energy Weatherization Assistance Program.

The weatherization assistance program works to help low income households meet their energy and weatherization needs. Click to the Department of Energy Weatherization Assistance webpage to determine eligibility and learn more.

What is Tennessee Weatherization Assistance Program?

“The Weatherization Assistance Program (WAP) is 100 percent federally funded through a grant from the Federal Department of Energy. The program provides funds to states to assist with the weatherization of the homes of low income elderly and disabled adults and families. The program is administered through contracts with an established network of 19 non-profit agencies and local governments experienced in providing weatherization services. WAP services are available in all 95 counties. Applicants must meet low-income eligibility guidelines based on established Federal poverty guidelines. Activities include: insulation, storm windows, caulking, and other related activities to reduce home energy costs and increase home energy efficiency.” [www.tn.gov]

While this information isn’t directly related to Tennessee insurance, the tips and benefits to be gained from weatherization will surely help in the areas of life, health, home and even auto. Now, to apply what I’ve learned and not procrastinate checking on these things until tomorrow…or next summer. Or next winter. Time moves quickly.

Not just for you . . .Long-Term Care Insurance is also for the people who would take care of you without it.

This is a professional blog.

But this is going to get personal.

I haven’t written a blog post since August. I couldn’t find the words in September. Since my dad’s health faltered to a point that he nearly died in the hospital. Since I struggled every day to help my mom find important documents and pertinent information. He was not cognitively aware or able to help. I had to dig through piles of disorganized papers and discovered more than a daughter should know, frankly. I’ll do my best to steer clear of that rabbit hole. It’s not a fun trip and won’t help anyone. This post is about an insurance topic that will affect every reader, in one way or another, if you or someone you love lives long enough.

Immediately following my dad’s hospitalization, my family quickly realized we were out of our depths and contacted a law firm that specializes in elder care. They have been a lifeline for me and I highly recommend consulting with experts early so that you aren’t to the point of drowning before reaching out for help. Perhaps, you have already made your own arrangements so your loved ones don’t have to scramble behind the scenes. Kudos to you. A thousand gold stars. My husband and I are committed to taking the steps necessary so our kids will not be handed the burden of responsibility for our care. Since they are teenagers, that’s hard to imagine, but long-term care requirements don’t only arise with old age.

[A current status report feels necessary to avoid unwarranted suspense. My dad mostly recovered and is receiving home healthcare after a twenty-day stay in a rehab facility last month. His diagnosis remains unclear, however through this experience, I can testify to the importance of having Long-Term Care insurance regardless of an individual’s prognosis.]

At the hospital with my dad.

No one enjoys taking photos during a difficult time. It isn’t fun to experience the first time around, so you don’t relish going down a visual memory lane later. I feel anxious just seeing the bed, the blood pressure cuff, the bland wall, and my dad lying under a thin blanket in a snap off gown like the one I wore when my children were born. I have this one because I like sending selfies to my teenage kids instead of tediously texting an update: “I’m with Pappaw at the hospital. It’s fine. He’s sleeping. Covid regulations in effect so I have to wear a mask.” Not quite 1000 words, but they get the picture. Pun intended.

We transferred my dad to a rehab facility covered by insurance for at least twenty days. An assessment would be made at the three week mark to determine if insurance would continue coverage. We–my mom, sisters and I–did not know the system and an acquaintance recommended we contact an elder care law firm to help us navigate “the game.” We had a preliminary consultation with a lawyer on Thursday, heard he was being discharged on Friday, registered an appeal on Saturday, prayed on Sunday, and brought him home Monday. The physician believed he was well enough to move on and insurance will not pay 100% for further therapy at that point. The aversion to paying out-of-pocket costs made us move quicker than we should have because if he had stayed, then he could have been transported to either assisted living or a nursing home. Since he returned home, he would not be considered at either place without going through hospitalization again. I’m not sure if it’s strictly Covid-19 protocol related, or the open beds are just that scarce. Because he doesn’t have Long-Term Care insurance, his options were extremely limited as those available are extremely expensive.

How does Long-Term Care insurance work?

To buy a long-term care insurance policy, you fill out an application and answer health questions. The insurer may ask to see medical records and interview you by phone or face to face.

You choose the amount of coverage you want. The policies usually cap the amount paid out per day and the amount paid during your lifetime.

Once you’re approved for coverage and the policy is issued, you begin paying premiums.

Under most long-term care policies, you’re eligible for benefits when you can’t do at least two out of six “activities of daily living,” called ADLs, on your own or you suffer from dementia or other cognitive impairment.

The activities of daily living are:

Bathing

Caring for incontinence

Dressing

Eating

Toileting (getting on or off the toilet)

Transferring (getting in or out of a bed or a chair)

A long-term care insurance policy helps cover the costs of that care when you have a chronic medical condition, a disability or a disorder such as Alzheimer’s disease. Most policies will reimburse you for care given in a variety of places, such as:

Your home

A nursing home

An assisted living facility

An adult day care center

Considering long-term care costs is an important part of any long-range financial plan, especially in your 50s and beyond. Waiting until you need care to buy coverage isn’t an option. You won’t qualify for long-term care insurance if you already have a debilitating condition. Most people with long-term care insurance buy it in their mid-50s to mid-60s.

The rates you pay depend on a variety of things, including:

Your age and health: The older you are and the more health problems you have, the more you’ll pay when you buy a policy.

Gender: Women generally pay more than men because they live longer and have a greater chance of making long-term care insurance claims.

Marital status: Premiums are lower for married people than for single people.

Insurance company: Prices for the same amount of coverage will vary among insurance companies. That’s why it’s important to compare quotes from different carriers.

Amount of coverage: You’ll pay more for richer coverage, such as higher limits on the daily and lifetime benefits, cost-of-living adjustments to protect against inflation, shorter elimination periods, and fewer restrictions on the types of care covered.

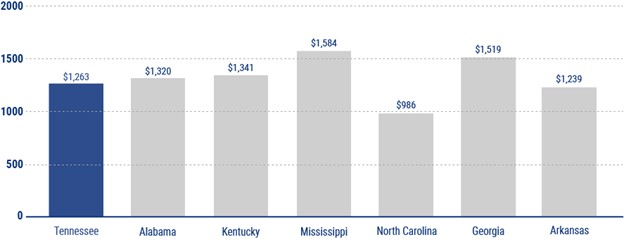

Tennessee has a higher cost of care than several neighboring states, with nursing homes averaging over $200/day, and as high as $240/day in several cities. The cost in Tennessee for home care and assisted care is approximately half as expensive, but still costly and well above what many could comfortably afford to pay, especially for an extended time period.

According to Tennessee Long Term Care Insurance Consultants, someone turning age 65 today has about a 70 percent chance of needing some type of long-term care during their lifetime. While one-third may never need long term care, 20 percent will need it for longer than 5 years. The average length of time people need long term care services is 3 years.1

In Tennessee, the average cost for 3 years of long term care is $274,299 ($91,433 per year) at 2020 rates. That cost is projected to be $495,414 ($165,138 per year) in 2040.2

And it’s not only seniors that need long-term care. Over 35 percent of people currently receiving long term care services are between 18 and 64.3

1. 2020 U.S. Department of Health and Human Services (www.longtermcare.acl.gov), site accessed 09/30/2021 2. Cost of Care Survey 2020 (Genworth.com), site accessed 09/30/2021 3. Family Caregiver Alliance (www.caregiver.org), site accessed 09/30/2021

The Tennessee Long Term Care Partnership Program is a special Tennessee program combining private long term care insurance with special access to Tennessee’s Medicaid Program (TennCare). The Tennessee Long Term Care Partnership helps Tennesseans prepare for the possibility of needing nursing home care, assisted living care or home care.

A Tennessee Long Term Care Partnership Program policy allows you to keep all, or part of your assets under the Medicaid program, if your long term care needs last longer than the benefits of your Partnership policy. Tennessee Legislature created the Tennessee Long Term Care Partnership under the auspices of several state government agencies.

Tennessee Long Term Care Partnership rates are like other policies. But the mandatory age-related inflation protection can increase the cost of insurance. So we recommend you compare Tennessee Long Term Care Partnership policies with regular LTC insurance. Because, you may find a wider range of choices better suited to your needs. This includes hybrid long term care insurance options not available under the Tennessee Long Term Care Partnership Program.

Happily Ever After – my parents, 1964

The photo above shows two kids, well, young adults at 20 and 23 years old, just married without a care in the world. The groom would be a high school teacher until becoming a licensed life insurance agent a few years later, and the bride would be a stay-at-home mother just a year later (when my oldest sister was born). They couldn’t imagine what the next 55+ years would bring, and despite his training, my insurance salesman father probably couldn’t imagine not having policies in place when he needed them the most. You just never know.

They say lightning never strikes the same place twice; they’re wrong.

What are the chances, right? The other day, out of the nearly clear blue sky, lightning struck my friend’s pool and knocked out their electronic circuit boards, HVAC system and DirecTV. She is lucky the damage wasn’t worse. Well, lucky may not be the right word, but they were fortunate a fire didn’t start and no one was electrocuted. Everything they lost could be replaced and they have homeowners insurance that would cover the losses.

For the fourth consecutive year, the number of lightning-caused U.S. homeowners insurance claims decreased in 2020 yet the average cost of those claims more than doubled since 2017, according to the Insurance Information Institute (www.iii.org).

The number of lightning caused claims fell 6.9 percent to 71,551 claims in 2020 from 76,860 in 2019, while the value of those claims soared 124.6 percent from $920.1 million in 2019 to $2.1 billion in 2020. Lightning-related homeowners insurance claim costs nationally rose dramatically due to a series of lightning strikes across Northern California in 2020, according to the Triple-I. The average cost per lightning claim in California was $217,555 last year while the national average was $28,885 in 2020, up 141.3 percent from $11,971 in 2019.

This tree was struck in my parents’ front yard a couple of years ago. The tree had to be cut down, but again, thankful that the lightning didn’t start a fire and cause more damage.

The Impact of a Lightning Strike (from NationalGeographic.com)

“Lightning is not only spectacular, it’s dangerous. About 2,000 people are killed worldwide by lightning each year. Hundreds more survive strikes but suffer from a variety of lasting symptoms, including memory loss, dizziness, weakness, numbness, and other life-altering ailments. Strikes can cause cardiac arrest and severe burns, but 9 of every 10 people survive. The average American has about a 1 in 5,000 chance of being struck by lightning during a lifetime.

Lightning’s extreme heat will vaporize the water inside a tree, creating steam that may blow the tree apart. Cars are havens from lightning—but not for the reason that most believe. Tires conduct current, as do metal frames that carry a charge harmlessly to the ground.

Many houses are grounded by rods and other protection that conduct a lightning bolt’s electricity harmlessly to the ground. Homes may also be inadvertently grounded by plumbing, gutters, or other materials. Grounded buildings offer protection, but occupants who touch running water or use a landline phone may be shocked by conducted electricity.

What to Expect when filing a claim for lightning damage–from valuepenguin.com

After you file the claim, an adjuster will inspect the damage to your home.

If the cost to repair your home exceeds the deductible of your policy, you will need to make a decision whether to file a claim.

If you choose to file a claim, the adjuster will offer you a settlement for repairs.

You receive the settlement from your insurance company in two increments. The first half of the settlement to be used to begin making repairs. The second will be for the remaining cost of the repairs after they have been made. “If you are offered an on-the-spot settlement, you can accept the check right away,” Worters says. “Later on, if you find other damage, you can reopen the claim and file for an additional amount.”

When both your home’s structure and personal property are damaged, you generally receive two separate checks from your insurance company – one for each category of damage. You should also receive a separate check for additional living expenses you might incur if your home in not uninhabitable until repairs are made.

Note that most policies require claims to be filed within 60 days from the date of disaster.

It is important to note that comprehensive car insurance will cover your car if it’s damaged by a lightning strike. Always a good idea to check your deductible and speak with your agent before filing a claim.

Michael Scott from The Office

Hopefully, lightning won’t be in the area today. . .or black cats or ladders to walk under or broken mirrors. The scariest thought is not having home or auto insurance to cover you if something unexpected should happen. (I had to say it!)

To protect yourself and other drivers, you must carry liability and uninsured motorist insurance in Tennessee.

It’s expensive and there are so many more things you’d rather spend money on than auto insurance, but if you get pulled over or in an accident, the officer is going to ask for three things: License, registration and proof of insurance.

If you are caught driving without insurance in Tennessee, you may be charged with a Class C misdemeanor, which can result in fines or a suspended driver’s license requiring an SR-22 form to be reinstated. Ignoring the law to save money could end up costing you a whole lot more.

Since 2017, uninsured drivers in Tennessee will pay fines and risk losing their vehicle registration if they are unable to demonstrate proof of financial responsibility. A web-based program will verify insurance for all Tennessee drivers. These changes come as part of the James Lee Atwood Jr. Law.

If you are involved in an accident while uninsured, your charge will be bumped up to a Class A misdemeanor. Penalties for driving without insurance can include:

A fine of $300

The revocation of your driver’s license until you:

Provide proof of insurance, and

Retake and pass your driver’s license examination

A restoration fee of $65 to get your license back

A $50 fee to be paid to the commissioner of safety

The requirement to provide proof of insurance with an SR-22 certificate for three years

Despite these consequences, about 20% of all motorists in this state are driving uninsured vehicles. This is much higher than the national rate of 13%.

In the state of Tennessee, your car insurance policy must include the following:

Liability insurance: This covers injuries and damage you may cause to others if you are responsible for a collision. You must have at least the following amounts of coverage:

Bodily injury liability coverage: $25,000 per person / $50,000 per accident

Property damage liability coverage: $15,000

Uninsured motorist insurance: This covers your injuries and property damage if you are in an accident caused by an uninsured, underinsured or hit-and-run driver. You must have at least the following amounts of coverage:

Bodily injury coverage: $25,000 per person / $50,000 per accident

Property damage coverage: $15,000

In addition to the mandatory coverage, most car insurance providers offer a variety of coverage options that you may want to consider. These include:

Collision coverage: This covers collision-related damage to your own vehicle, regardless of fault. Pays to repair or replace your car if it is damaged in a collision with another vehicle or a stationary object. It can also cover you if you overturn your vehicle while making a sharp turn. It is often required by lenders until you have paid off your vehicle.

Comprehensive coverage: This covers non-collision-related damage to your own vehicle if it is lost or damaged due to an event such as a falling object, flood, structure fire, hailstorm, or property crime including car theft. This is also typically required by lenders until you have paid off your vehicle.

Medical payments coverage aka Personal injury protection (PIP): This provides coverage for your own medical bills if you (and your passengers) are injured in an accident, regardless of fault.

Towing and roadside assistance: This covers the cost of assistance if your vehicle becomes disabled while you are out on the road, such as if your engine overheats or you get a flat tire.

Rental car reimbursement: This can cover the cost to rent a vehicle while your own vehicle is being repaired following a covered event.

Vehicle owners in Tennessee pay an average of $1,186 per year for their auto insurance coverage. This is lower than the national average of $1,311. Your actual quoted price for coverage will be calculated based on factors such as the make, model, trim, and year of your car, and even personal details like your driving history, age, occupation, and credit score. Comparing quotes from a variety of insurers lets you be sure that you are getting the coverage you want at a competitive price.

Car insurance policies in Tennessee generally follow the car rather than the individual. For example, if you get in a car accident while driving a friend’s vehicle, the primary source of the compensation would be your friend’s auto insurance coverage, not your own.

Tennessee is not a no-fault state.

This means that if you are in a collision, the person responsible for the accident is responsible for covering any resultant property damage and necessary medical treatment. If the at-fault driver does not have enough insurance to cover the costs, they will be expected to make up the difference out of pocket.

In no-fault states, your own insurance policy provides the first line of coverage for necessary medical treatment, regardless of fault.

When seeking to reinstate your driver’s license after being convicted of a DUI, driving without insurance, reckless driving, or another driving violation that results in a suspension, you must file a SR-22 insurance document. This form gives proof of future responsibility, and you might need to have it for five years from the date of the suspension.

According to the Tennessee Department of Safety and Homeland Security, if you file the SR-22 for a total of three years within the five-year period, the SR-22 might be canceled. If five years pass from the date of the suspension before you reinstate your privileges, then you don’ need to file the SR-22. If you cancel the SR-22 before the required time passes and you fail to file a new form, your driving privileges remain suspended.

Your insurance provider may be able to electronically file the SR-22 insurance documents. That way, you can get back on the road quicker, though with a little less cash in the bank.

With piracy active in digital waters, cyber attacks are on the rise and Cyber Liability Insurance is more important than ever.

The Russians are coming, the Russians are coming! That movie is before my time, but watch the nightly news and it seems Putin and his posse of cyber terrorists are constantly on the attack. Whether he is leading the charge or not, we have seen a dramatic increase in malicious attempts to damage or disrupt computer networks through data breaches, ransomware, fraud and Denial of Service (DoS) attacks. Most people are familiar with computer viruses now and know not to click on a suspicious link emailed to fifty of their closest friends, but rather than a costly appointment with a Geek Squad member, these attacks can be significant. Just last month, we saw what happens when a gas company’s computer system is compromised and held hostage for a short time. What would happen to your company or business if the computer system was taken hostage? What’s at stake?

“Online threats are varied and they don’t discriminate organizations from individuals when looking for a target. . .it’s not an exaggeration to say that cyber threats may affect the functioning of life as we know it.”

Software that performs a malicious task on a target device or network, e.g. corrupting data or taking over a system.

Phishing

An email-borne attack that involves tricking the email recipient into disclosing confidential information or downloading malware by clicking on a hyperlink in the message.

Spear Phishing

A more sophisticated form of phishing where the attacker learns about the victim and impersonates someone he or she knows and trusts.

“Man in the Middle” (MitM) attack

Where an attacker establishes a position between the sender and recipient of electronic messages and intercepts them, perhaps changing them in transit. The sender and recipient believe they are communicating directly with one another. A MitM attack might be used in the military to confuse an enemy.

Trojans

Named after the Trojan Horse of ancient Greek history, the Trojan is a type of malware that enters a target system looking like one thing, e.g. a standard piece of software, but then lets out the malicious code once inside the host system.

Ransomware

An attack that involves encrypting data on the target system and demanding a ransom in exchange for letting the user have access to the data again. These attacks range from low-level nuisances to serious incidents like the locking down of the entire city of Atlanta’s municipal government data in 2018.

Denial of Service attack or Distributed Denial of Service Attack (DDoS)

Where an attacker takes over many (perhaps thousands) of devices and uses them to invoke the functions of a target system, e.g. a website, causing it to crash from an overload of demand.

Attacks on IoT Devices

IoT devices like industrial sensors are vulnerable to multiple types of cyber threats. These include hackers taking over the device to make it part of a DDoS attack and unauthorized access to data being collected by the device. Given their numbers, geographic distribution, and frequently out-of-date operating systems, IoT devices are a prime target for malicious actors.

Data Breaches

A data breach is a theft of data by a malicious actor. Motives for data breaches include crime (i.e. identity theft), a desire to embarrass an institution (e.g. Edward Snowden or the DNC hack), and espionage.

Malware on Mobile Apps

Mobile devices are vulnerable to malware attacks just like other computing hardware. Attackers may embed malware in app downloads, mobile websites, or phishing emails and text messages. Once compromised, a mobile device can give the malicious actor access to personal information, location data, financial accounts, and more.

If your computer systems are hacked or customer, employee or partner data is otherwise lost, stolen or compromised, the costs of response and remediation can be significant. According to iii.com, your business may be exposed to the following costs:

Liability—You may be liable for costs incurred by customers and other third parties as a result of a cyber attack or other IT-related incident.

System recovery—Repairing or replacing computer systems or lost data can result in significant costs. In addition, your company may not be able to remain operational while your system is down, resulting in further losses.

Notification expenses—In several states, if your business stores customer data, you’re required to notify customers if a data breach has occurred or is even just suspected. This can be quite costly, especially if you have a large number of customers.

Regulatory fines—Several federal and state regulations require businesses and organizations to protect consumer data. If a data breach results from your business’s failure to meet compliance requirements, you may incur substantial fines.

Class action lawsuits—Large-scale data breaches have led to class action lawsuits filed on behalf of customers whose data and privacy were compromised.

What cyber liability insurance covers

Some standard business insurance policies, such as a Business Owners Policy (BOP), may provide coverage for certain types of cyber incidents and may pay recovery or replacement costs. To extend coverage for a fuller range of cyber liability risks, you will need to purchase a stand-alone cyber liability policy, customized for your business. This type of policy can cover several types of risk, including:

Loss or corruption of data.

Business interruption.

Multiple types of liability.

Identity theft.

Cyber extortion.

Reputation recovery.

Steps to reduce cyber liability risks

Installing, maintaining and updating security software and hardware.

Contracting with an IT security services vendor.

Using cloud computing services.

Developing, following and publicly posting a data privacy policy.

Regularly backing up data at a secure offsite location.

New Cybersecurity Law in Tennessee Takes Effect July 1, 2021

Friday, May 21, 2021 | 10:28am | tn.gov

NASHVILLE — Tennessee insurance consumers will gain new protections for their personal, medical and financial information with the recent passage by the Tennessee General Assembly of the Insurance Data Security Law. Signed by Tennessee Governor Bill Lee, the law takes effect July 1, 2021.

“Tennessee’s adoption of the bill is critical for the Commissioner and the Department to have the tools they need to better protect Tennesseans’ sensitive consumer information.”

Assistant Commissioner for Insurance, Bill Huddleston.

The law modernizes, defines and toughens existing security measures that Tennessee insurance carriers must take to protect consumer information. Under the new law, insurance carriers must:

Identify internal or external threats that could result in unauthorized access, transmission, disclosure, misuse or destruction of consumers’ private information.

Develop, implement and maintain an information security program based on its individual risk assessment with a designated employee in charge of the information security program.

Investigate any cybersecurity breach and notify the Insurance Commissioner of a cybersecurity event if the licensee is a domiciled insurer or if more than 250 Tennesseans are impacted.

Spearheaded by the National Association of Insurance Commissioners (NAIC), the creation of model legislation that formed the basis for Tennessee’s law was created with the input of national regulators after a succession of data breaches exposed millions of Americans’ personal information. The NAIC made cybersecurity and consumer data protection top priorities. The model legislation was the result of a two year collaborative process that resulted in a model law that could be adopted by various states.

In an effort to raise greater awareness among consumers about cybersecurity, TDCI reminds consumers to familiarize themselves with the NAIC’s Cybersecurity Consumer Protections.

As an insurance consumer, you have the right to:

Know the types of personal information collected and stored by your insurance company, agent or any business it contracts with (such as marketers and data warehouses).

Expect insurance companies/agencies to have a privacy policy posted on their websites and available in hard copy, if you ask. The privacy policy should explain what personal information they collect, what choices consumers have about their data, how consumers can see and change/correct their data if needed, how the data is stored/protected, and what consumers can do if the company/agency does not follow its privacy policy.

Expect your insurance company, agent or any business it contracts with to take reasonable steps to keep unauthorized persons from seeing, stealing or using your personal information.

Get a notice from your insurance company, agent or any business it contracts with if an unauthorized person has (or likely has) seen, stolen or used your personal information. This is called a data breach. This notice should: • Be sent in writing by first-class mail or by e-mail. • Be sent soon after a data breach and never more than 60 days after a data breach is discovered. • Describe the type of information involved in a data breach and the steps you can take to protect yourself from identity theft or fraud. • Describe the action(s) the insurance company, agent or business it contracts with has taken to keep your personal information safe. • Include contact information for the three nationwide credit bureaus. • Include contact information for the company or agent involved in a data breach.

Get at least one year of identity theft protection paid for by the company or agent involved in a data breach.

If someone steals your identity, you have a right to: • Put a 90-day initial fraud alert on your credit reports. (The first credit bureau you contact will alert the other two.) • Put a seven-year extended fraud alert on your credit reports. • Put a credit freeze on your credit report. • Get a free copy of your credit report from each credit bureau. • Get fraudulent information related to the data breach removed (or “blocked”) from your credit reports. • Dispute fraudulent or wrong information on your credit reports. • Stop creditors and debt collectors from reporting fraudulent accounts related to the data breach. • Get copies of documents related to the identity theft. • Stop a debt collector from contacting you.

To learn more about the protections in your state or territory, contact your consumer protection office at:

Questions about your insurance policy or need to file a complaint? Contact the TDCI team at 1-800-342-4029 or 615-741-2218.

Standard Definitions Under This Bill of Rights Data Breach: When an unauthorized individual or organization sees, steals or uses sensitive, protected or confidential information—usually personal, financial and/or health information.

Credit Bureau (Consumer Reporting Agency): A business that prepares credit reports for a fee and provides those reports to consumers and businesses; its information sources are primarily other businesses.

Credit Freeze (Security Freeze): A way you can restrict access to your credit report and prevent anyone other than you from using your credit information.

Personal Information (Personally Identifiable Information): Any information about a consumer that an insurance company, its agents or any business it contracts with maintains that can be used to identify a consumer. Examples include: • Full name. • Social Security number. • Date and place of birth. • Mother’s maiden name. • Biometric records. • Driver’s license number.

Why Protecting your Toys this Spring and Summer is Essential

Your Homeowners policy does cover personal property, but what is kept in the home, and not for the full amount it would cost to replace or repair the item in case of an accident or loss. (See the difference between Actual Cash Value and Replacement Cost.) Consider what you own that is not covered by your Homeowners policy and protect those expensive toys from damage that is almost inevitable.

Spring has sprung! Bradford Pear trees have bloomed and boating in East Tennessee is starting to pick up. Like those trees, a day on the water is beautiful, but can be stinky if the wind shifts and an accident happens. If you know, you know.

So, what does personal property include?

The contents of your home are your personal property. This includes furniture, appliances and clothing. Not all personal property is covered. Items more appropriately covered under different forms of insurance may have limited or no coverage for loss. These items include, but are not limited to, money, jewelry and firearms.

“Insurance agents and brokers should work with clients to find a valuable articles policy that offers worldwide protection with no deductible, automatic coverage for new items, and an agreed value feature with a market value enhancement. In the event of a covered total loss, clients will get 100% of the agreed value as a cash settlement, and if the market value of the item has increased, clients may benefit from inflation protection up to 150% of the itemized value, up to the policy limit.”

Laura Doyle, excerpt from the Insurance Journal magazine, August 2020

Property damage liability—Property damage liability insurance covers the cost of damages to someone else’s property after an accident you cause. In most cases, your property damage will pay out when you are at fault for an accident that causes damage to someone else’s boat or PWC.

Collision damage—When your boat or PWC is damaged in an accident, collision insurance is an optional coverage that pays the cost of repairing or replacing it, minus the amount of your deductible.

Bodily injury liability—Bodily injury liability coverage is the part of your insurance policy that pays for the costs associated with injuries to other people involved, if you are found legally responsible for a boating accident.

Hull coverage—Hull insurance covers any physical damages that occur to your boat and generally includes trailers, equipment, motors, and accessories. Typical claims include fire and windstorm damage.

Fuel spill liability—A separate policy that separates out fuel spill liability and provides coverage for any fines that may occur from an accident involving a fuel spill.

Here are some tips to ensure that you are getting your money’s worth and keeping your costs down:

Only buy what you need: There are lots of options out there for marine insurance and many of these policies are custom-written. Ensure that you know what you need so you can avoid paying for features that you don’t require.

Agreed value vs. Cash value: In an agreed value policy, you are paid a pre-determined value for the vessel in the event of a total covered loss. With agreed value, the insured and insurer agree on the value of the boat upfront. Most agents would recommend this option for a new or late-model boat. As the boat continues to age, look to potentially switch to a cash value option to save on premiums.

Take a boater safety course: Almost all insurers offer a discount for boaters that have recently completed an approved boater safety course. Take an in-person class or get your boat safety certification online. Check with your insurance agent to see if a discount is offered for your specific policy.

Spend on safety gear: Insurance companies may cut you an additional discount for having extra safety features onboard your vessel. Check with your insurance agent to see if you qualify for any additional savings.

The 8 Best Boat Insurance Providers of 2021

Best for Professional Fishermen: Markel.

Best for Affordability: Allstate.

Best for Safe Boat Drivers: Progressive.

Best for Additional Coverage Options: Foremost.

Best for Policy Bundling: Nationwide.

Best for Individualized Customer Service: United Marine Underwriters.

Best for Emergency Services Coverage: State Farm.

The type of boat, its length, and its expected use will largely dictate your boat insurance rates. Whether you have a speed boat, a small fishing boat, or a yacht will make a big difference in what you pay. In general, boat insurance costs typically range from $200 to $500 per year, on average. The amount of boat insurance you may need depends on a number of factors, including the boat’s value, motor size, and age. Like other vehicles, high-performance boats will likely command a higher level of coverage to compensate for the amount of damage they are able to inflict.

Even though Tennessee does not require boat insurance, it is quite useful in the event of loss from theft, fire, storm damage, and many other threats. One of the most convenient ways of paying for your boat insurance is by bundling it with your current auto or home insurance. You can often save a significant amount of money by doing so and all it takes is one loss to more than pay for the difference.

If you plan on keeping your boat at a marina, it’s likely you willbe required to carry boat insurance. A marina with multiple docks is a prime spot for large and small vessels to collide and cause damage.

One great hazard—even if you have a solid boat-insurance policy—is damage caused by other, uninsured boaters. So sometimes having uninsured-boater protection in your policy can be as important as protection from liability damage, especially in a state like Tennessee, where boat insurance is not mandated by law.

An important note: Be sure to ask whether tow insurance is covered by your plan. This aspect of boat insurance is often sold as a separate package, but it may not be required if towing is already covered by your policy.

Also, be sure to know specifically where your insurance covers you. Many people don’t know that boat insurance will only cover you in specified waters, so be aware of drifting into international or coastal waters where your insurance may not cover you.

It’s nearly Memorial Day weekend–the unofficial start of summer–and we can hardly wait. Dust off the ATVs and jet-skis, fill the coolers and gas tanks, make sure life jackets still fit, and update your insurance policy today.

Talk to your agent to determine how changing your deductible could affect your bottom line.

A deductible is basically the amount you agree to pay in the event of a claim, either a specific dollar amount or a percentage of the total amount of insurance on the policy. For example, we have a $500 deductible on our auto insurance and a 1% deductible on our home insurance. True story, we just added our 16 year old son to the auto policy and his rate is rather high right out of the gate. I asked if it would save us money to increase the deductible to $1000 or more and the savings were not that large, like $6 a month, so I left it. At the three month mark of receiving his drivers license, my son wrecks his car. Thankfully, no injuries, but the claim is going to raise his already high rate even higher. Thankfully, no one was hurt. Yes, I repeated myself because I only feel better with the reminder that things could’ve been much worse. That $500 deductible doesn’t sting quite as much either, but it’s also something we’d prefer never to use. Alas, we have teenage drivers so it comes with the territory. We are glad everyone is okay and cars can be repaired. Still. . .

Ugh.

Back to deductibles. Good news is you get to choose your own. Tennessee has minimum car insurance requirements for bodily injury, property damage and uninsured motorist bodily injury:

Bodily injury liability: $25,000 per person and $50,000 per accident

Property damage liability: $15,000 per accident

Uninsured motorist bodily injury: $25,000 per person and $50,000 per accident*

Uninsured motorist property damage: $15,000 per accident*

*Note, deductibles are paid for each claim. So you can’t “hit your deductible” as we can do with health insurance.

If you have a loss that adds up to the amount near your deductible, first, always check with your agent, but most times you’re better off paying for the repair without filing a claim. Your insurance will increase and some companies will drop you after filing multiple claims, so you have other considerations besides reimbursement.

“Take a new look at your deductibles for car and homeowners insurance,” says Julie Murphy Casserly, CFP and author of “The Emotion Behind Money.”

“See if you’ve built up enough savings so that you don’t need a $250 deductible but can go up to $1,500 deductible and decrease what you’re paying to your insurance company every month in premiums,” she says.

Increasing your deductible to $1,000 could reduce your premium by up to 25 percent and save money, she says. On a $500 premium, that could mean pocketing more than $100 in savings this year. [Excerpt from bankrate.com]

Finance and insurance analyst Laura Adams explains, “It’s important to know what [deductibles] are and when they apply to various claims. If you don’t have enough savings to pay a deductible after getting into a car accident or having a tree fall on your roof, you might not be able to complete needed repairs.”

YouGov Plc conducted a nationwide survey. In early September 2020, they gathered data from more than 2,800 Americans. This study found that over half (61%) of the property insurance policyholders surveyed are not very confident they know what their insurance deductible is for their policy. More than 78% of policyholders have some concern that they wouldn’t be able to afford the costs of a claim, and 36% wouldn’t be able to cover a claim using their savings.

That’s a problem. Scott Holeman, Media Relations Director at the Insurance Information Institute (III), says, “We offer this advice: Never take a higher deductible than you can afford. Choosing a high deductible can mean a lower monthly insurance payment, but it also means a higher bill to pay when things go wrong.”

Paying a little extra each month may be worth it to you to have a lower and easier to manage deductible, as in the case of covering a teenage driver, but if you are generally a safe driver and have funds to cover a higher deductible should you experience a loss, look into lowering that monthly premium. You get to decide, but asking your agent for advice is a good idea and it’s what they are there to do. Mike, Billie and Susan are here to answer any questions and review your deductibles with you.

How do you choose? By looks, by experience, by personality, by clever marketing swag? Consider these questions first.

Now that we’ve all celebrated (or hated) Valentine’s Day, let’s turn our focus to an oft overlooked relationship in our lives: the one with your insurance agent. Quick! What’s his/her name? If you know without looking, that’s a good start, but I should stop here to add that if you don’t know the carrier of your insurance, then you aren’t ready to speed date. You need to take it slow and start at the beginning. The following questions should be asked as soon as introductions are made because the answers could quickly reveal compatibility or lack thereof.

1. What’s your specialty?

At Herron-Connell, we write all lines of insurance: home, auto, life, health, business/commercial, disability, specialty, umbrella and more. You can see how having so many options could spread one person thin on their expertise level, so ask if your needs line up best with their qualifications. You may partner up with more than one person in an agency–it’s not cheating!

2. Are you an Independent Agent or a Direct Broker?

An independent agent is not monogamous. They aren’t committed to one particular insurance company so has a wider range of options and carriers to choose from that would ideally best benefit the customer. They can play the field, to keep the analogy going. A direct broker or a captive agent only represents a specific company, like State Farm, and they cannot shop around for a better rate or other options should you lose coverage or get dropped for multiple claims, for example. Herron-Connell is an independent agency and can mix & match if a combo package isn’t best for home and auto, or different carriers have lower rates in multiple areas.

3. Do I get any discounts?

Everyone wants to save a little money, but this question will also reveal the agent’s knowledge and willingness to help. If you feel like they don’t want to take the extra steps to save you money, or heaven forbid, give you any sort of evil eye, run. This dismissive treatment is a giant red flag flapping in the wind of a customer service desert. Discounts could include a good driver discount, a multi-policy discount for bundling home & auto, a lifestyle change; it is a matter of asking and clicking boxes on the application, not very time-consuming or labor-intensive.

4. What’s your home number?

Just kidding, that’s a little much, but ask what you should do if/when you have a question or need help after office hours. Insurance incidents don’t only occur during the week between 9-5. Whether you have a car accident, need help getting a claim paid or something less urgent but important, your agent should be available and willing. When they are not accessible for any reason, they should provide after-hours contact information so that when you need assistance, you have options.

5. Got any references?

Considering all of the personal information your insurance agent asks you, it is completely reasonable, nay, responsible of you to ask them for client references. They may have nailed the interview or first impression, but what happens the day after. Will they take your call? Will they even remember your name? What others say about them counts much more than what they say about themselves. If the words trustworthy, helpful, knowledgeable never show up, them you should probably ring the bell and move on.

If you aren’t comfortable asking these questions, try emailing them to the prospect. This relationship is important and should not be one-sided. Hopefully, if all goes well, you will only hear from them before time comes for renewal or if you run into them at a ballgame or some place. But, taking the time to ask these questions before you make a long-term commitment can help avoid unnecessary heartache and frustration later.